SpaceX IPO Roadshow: From Launch Provider to Space, Connectivity, and AI Infrastructure Platform

The SpaceX roadshow does not sell a simple rocket company. It presents SpaceX as a physical infrastructure platform for the AI era: launch, Starlink connectivity, xAI/Grok, X data, terrestrial compute, and eventually orbital AI compute.

Bottom line: the SpaceX IPO story is not merely a space-company listing. It is a claim on physical infrastructure premium in the AI era. The key investor questions are Starship economics, Starlink capacity, AI compute monetization, and whether orbital AI compute can move from concept to evidence.

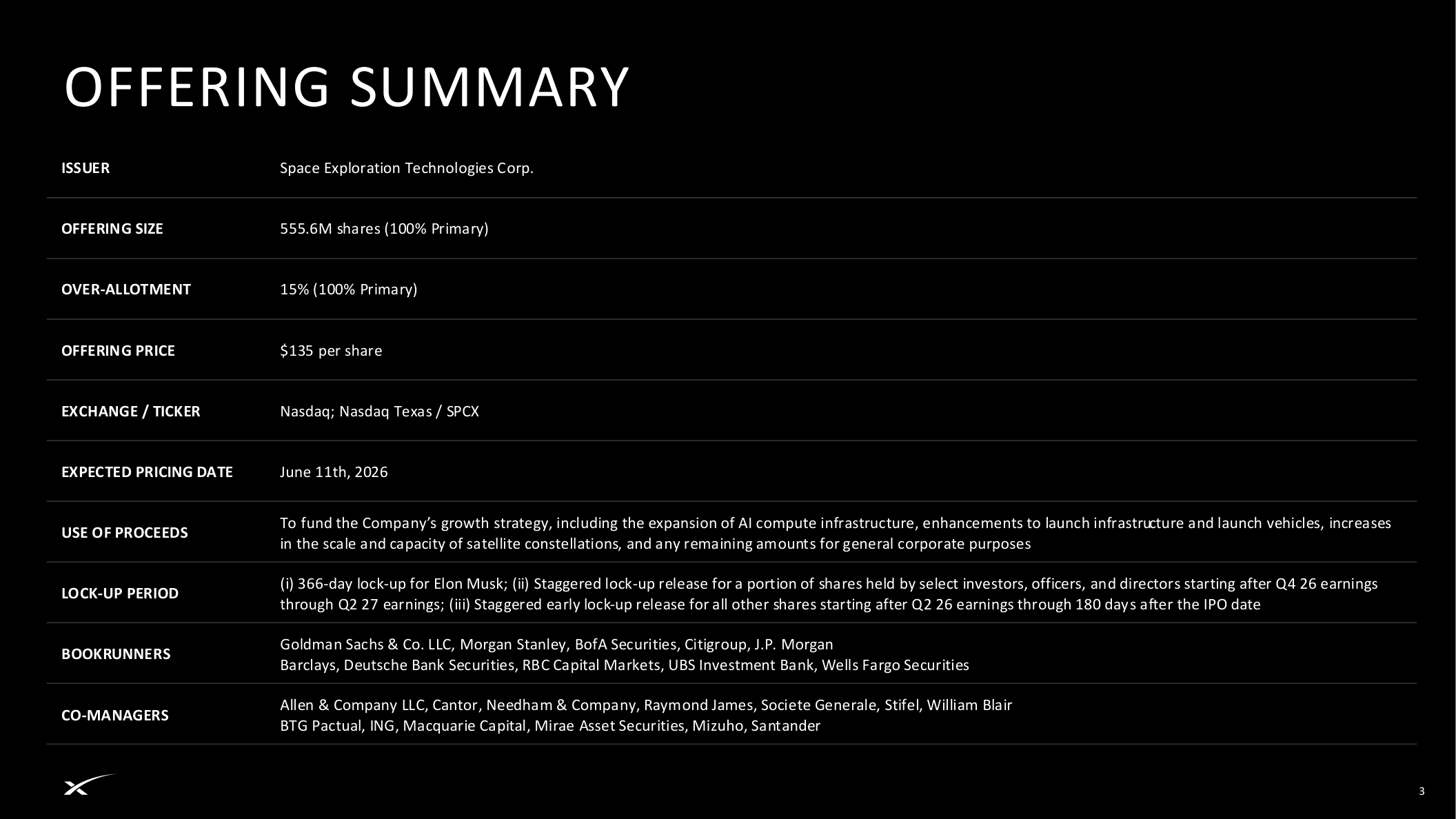

The offering is already massive

The PDF shows 555.6 million primary shares offered at $135 per share, implying roughly $75 billion of gross proceeds by simple multiplication. The expected listing venues are Nasdaq and Nasdaq Texas, under ticker SPCX, with expected pricing on June 11, 2026.

The use of proceeds matters. SpaceX points to expansion of AI compute infrastructure, improvements to launch infrastructure and vehicles, increased scale and capacity of satellite constellations, and general corporate purposes. In other words, the IPO capital is meant to fund the AI, launch, and satellite capex flywheel at the same time.

Supply still matters after listing

Elon Musk is subject to a 366-day lock-up, while selected investor, officer, and director shares have staged release schedules from late 2026 into 2027. Early scarcity may later meet lock-up supply events.

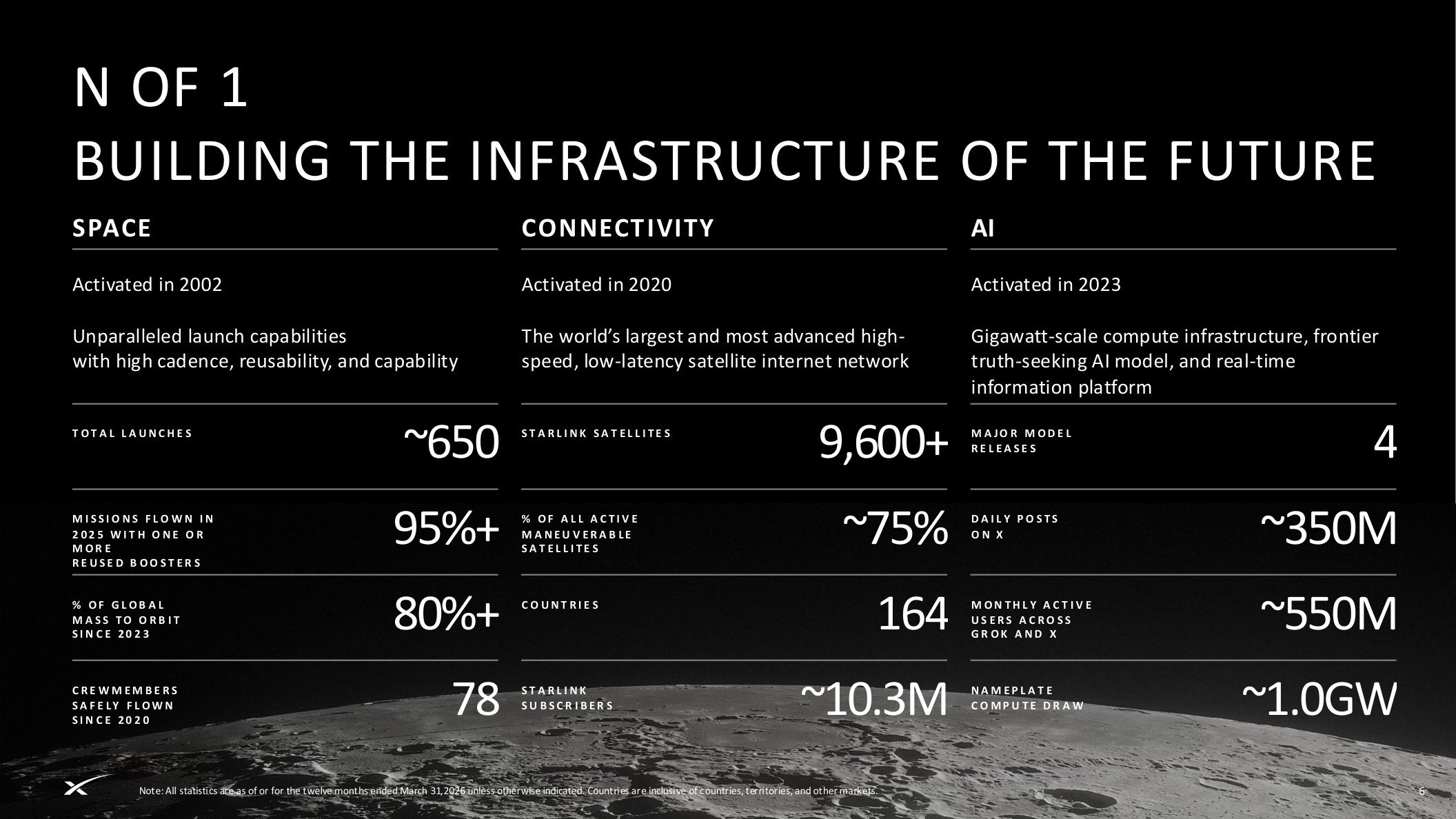

SpaceX is positioning itself as Space + Connectivity + AI

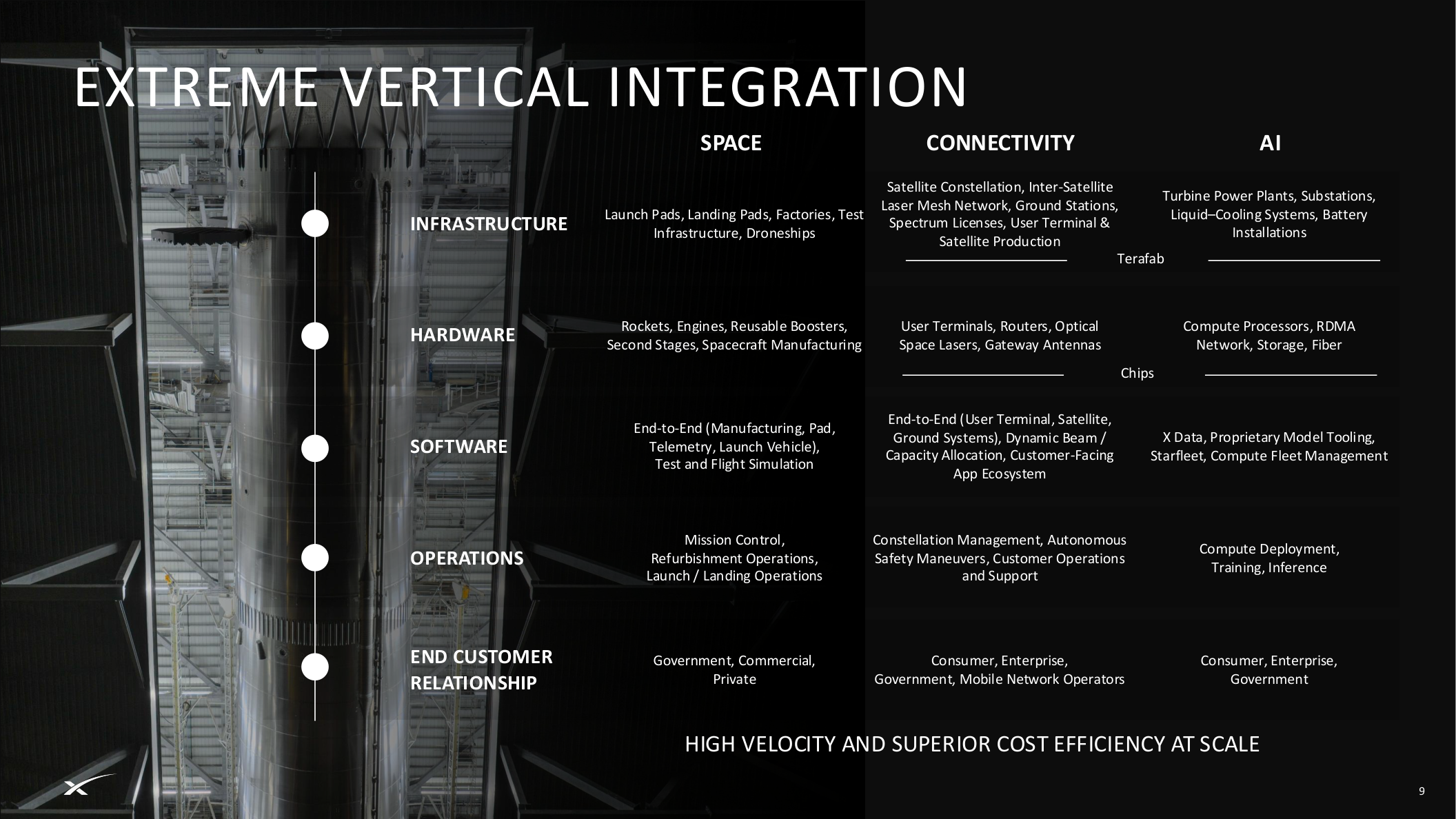

The roadshow defines SpaceX as integrated hardware and software infrastructure across space, connectivity, and AI. Space means reusable rockets and high launch cadence. Connectivity means Starlink broadband, satellite-to-mobile, enterprise, and government networks. AI means xAI/Grok, real-time X data, terrestrial compute, and eventually orbital compute.

The shared theme is vertical integration: launch pads, rockets, satellites, terminals, chips, power, cooling, data centers, software, operations, and customer relationships tied inside one platform.

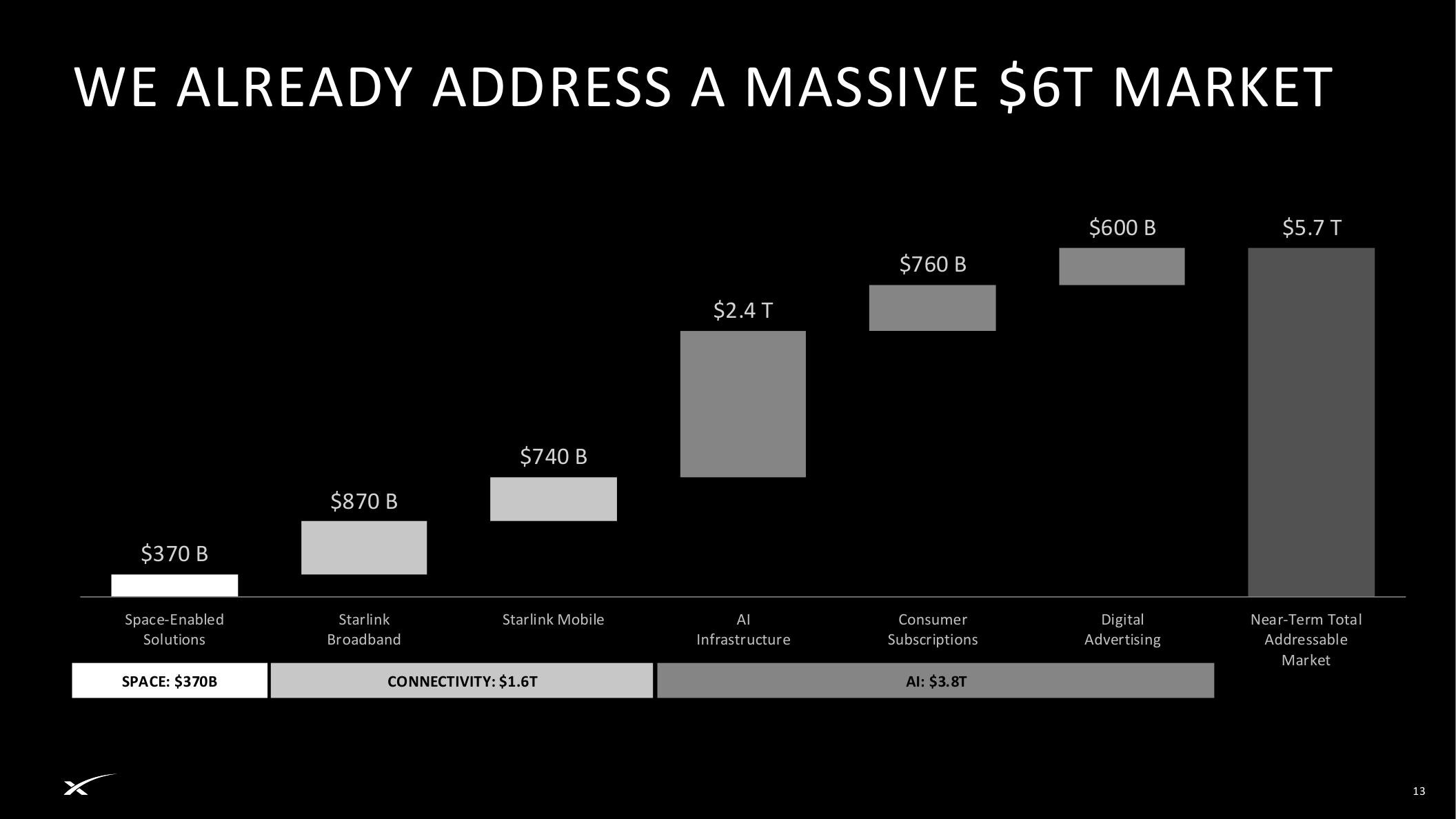

The roadshow frames a $5.7T near-term market and a larger AI option

SpaceX presents a near-term total addressable market of about $5.7 trillion: $370B for space-enabled solutions, $870B for Starlink Broadband, $740B for Starlink Mobile, $2.4T for AI infrastructure, $760B for consumer subscriptions, and $600B for digital advertising.

The larger premium comes from AI. The deck also frames the AI opportunity as potentially far larger, with AI TAM shown at $26.5T in the longer-run slide. That is not current revenue; it is the option value behind the premium.

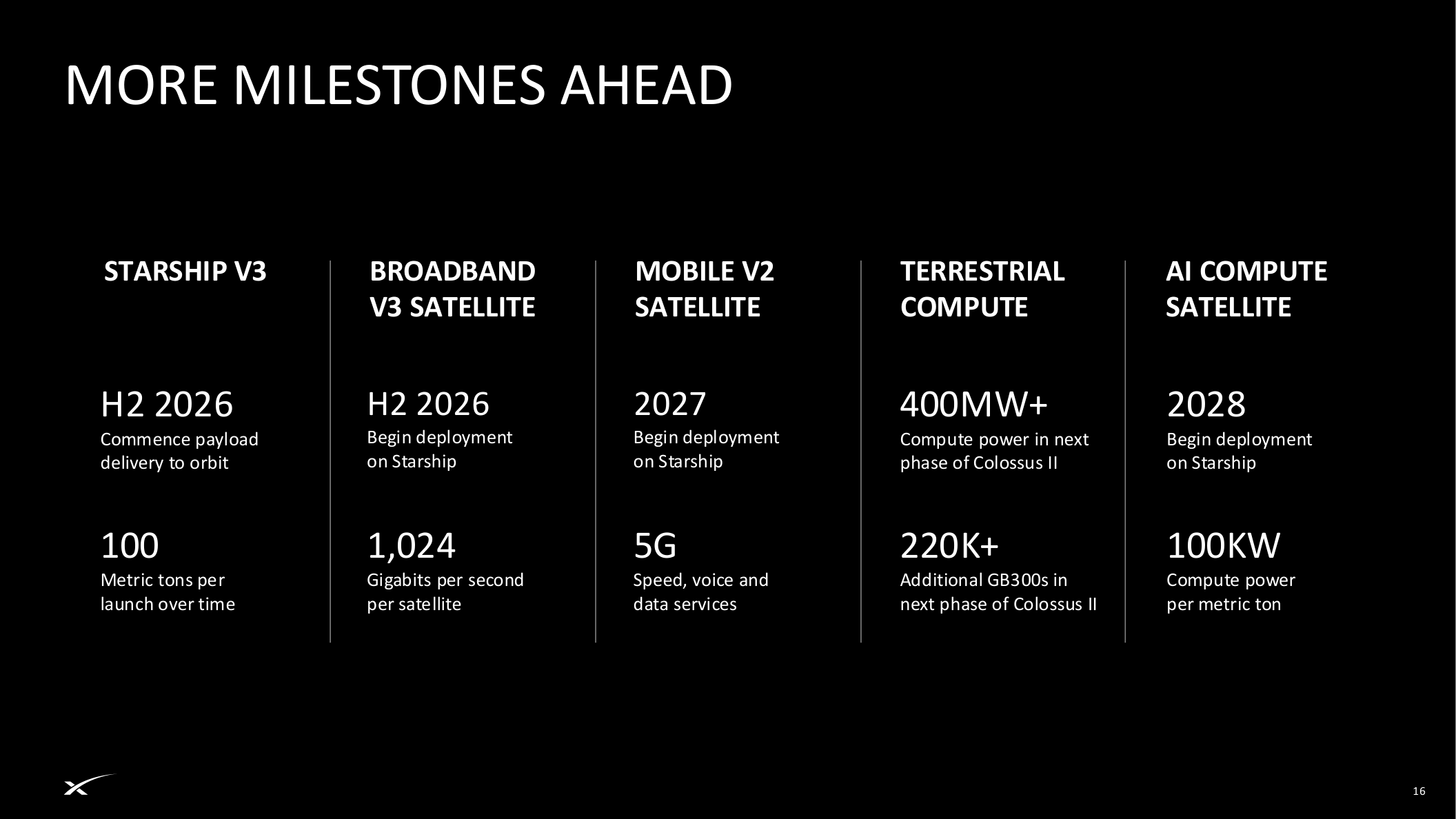

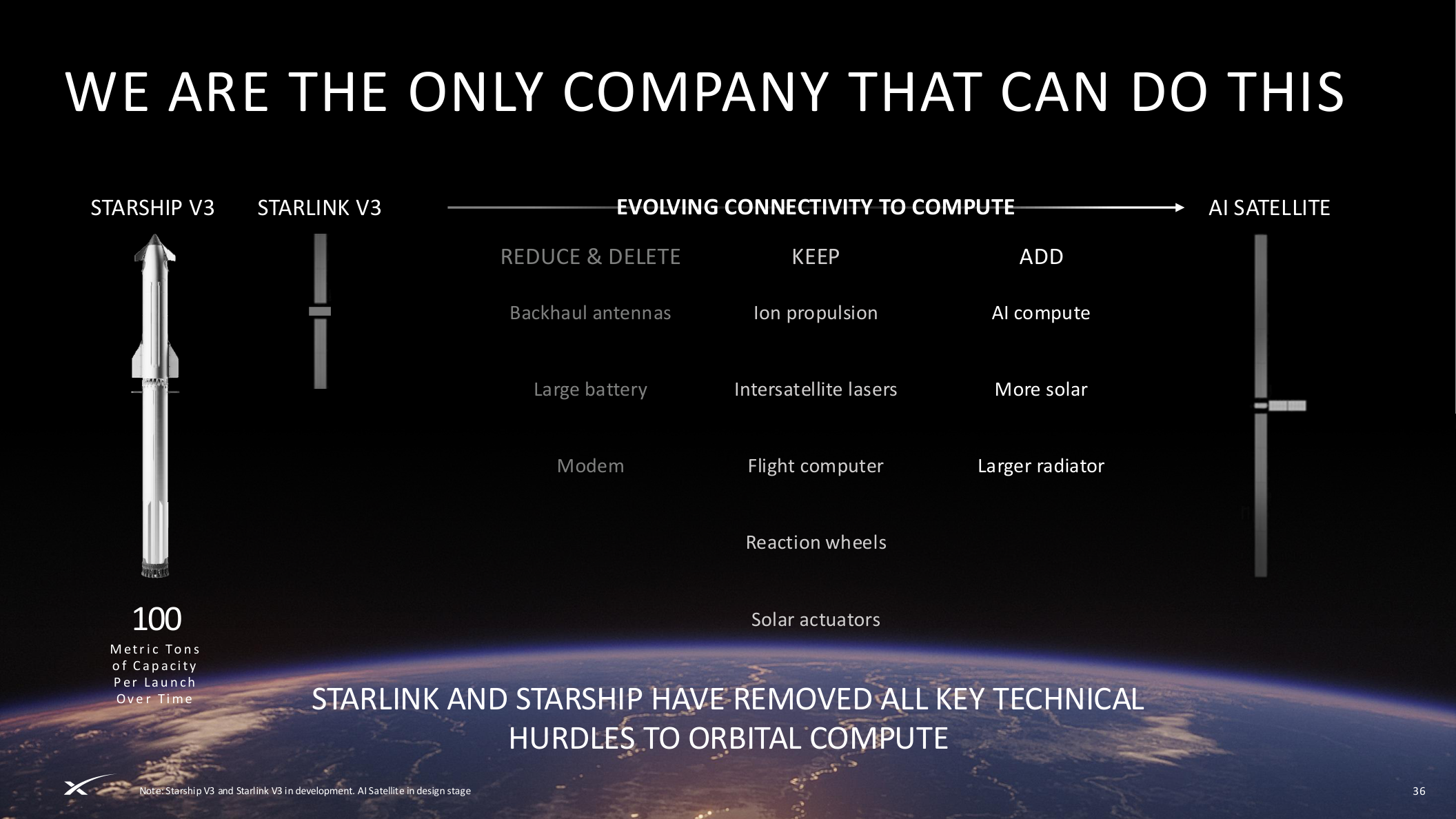

The 2026-2028 roadmap is built around Starship

Starship V3 payload delivery to orbit is targeted for the second half of 2026. Broadband V3 satellite deployment on Starship is also targeted for H2 2026, Mobile V2 satellite deployment for 2027, and AI compute satellite deployment for 2028. The next phase of Colossus II is presented at 400MW+ and 220K+ GB300s.

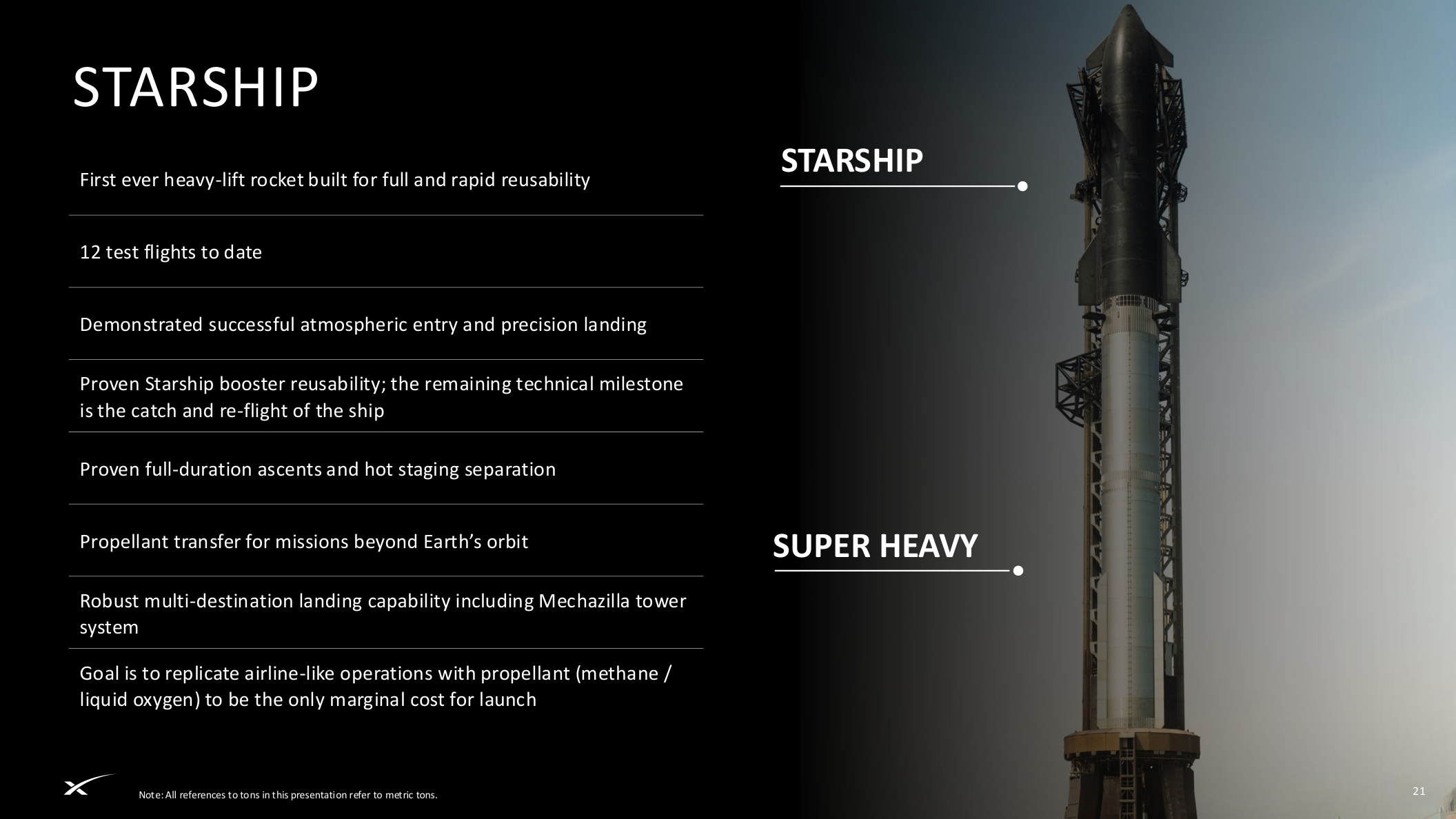

Reusable launch is the foundation of every other business

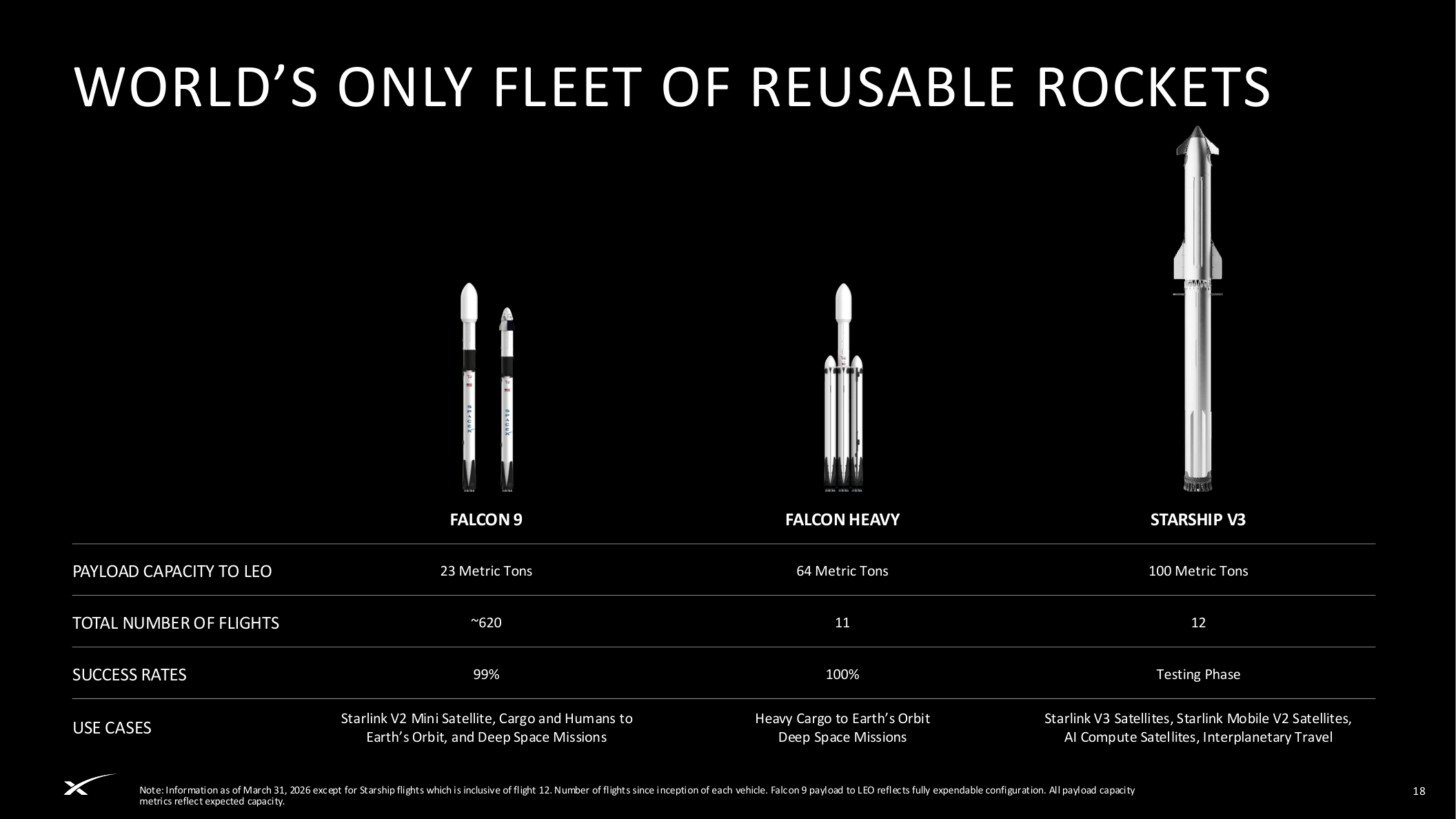

SpaceX claims more than 80% of global mass to orbit since 2023. Falcon 9 is shown at 23 metric tons to LEO, around 620 total flights, and a 99% success rate. Starship V3 is framed as a 100 metric ton platform for Starlink V3, Mobile V2, AI compute satellites, and interplanetary travel.

On cost, the deck compares historical LEO launch cost at $18,500 per kg, Falcon Heavy at $2,700, Falcon 9 at $1,400, and Starship as a 99%+ target cost-reduction platform. If that step-change becomes real, the cost curve for connectivity and AI infrastructure changes with it.

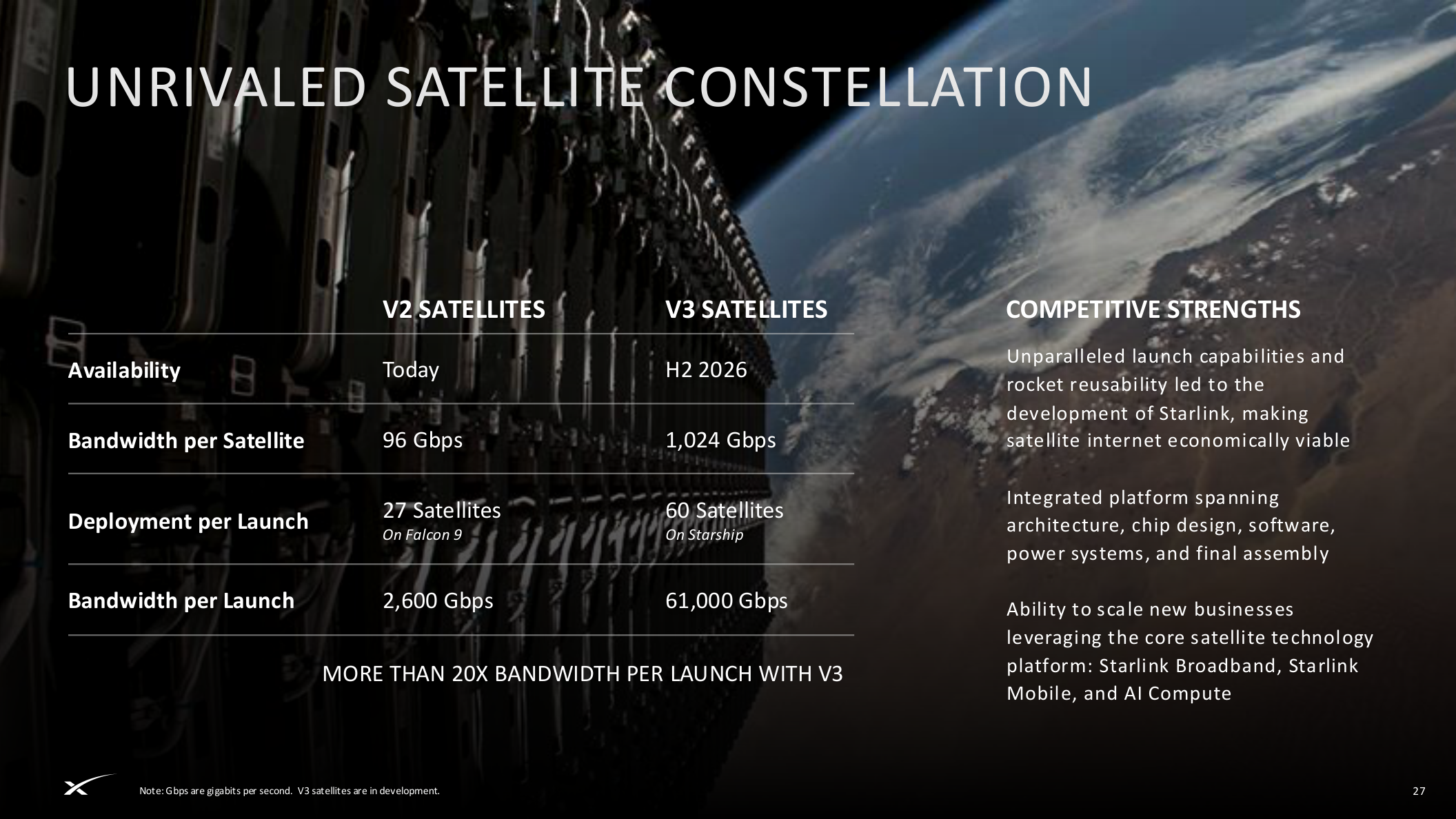

Starlink is already a scaled satellite internet platform

The deck cites 9,600+ Starlink satellites, roughly 75% of active maneuverable satellites, 3,000+ deployed in 2025, and 10.3M subscribers by Q1 2026. It also shows 3.3B+ people covered, 164 countries and markets, and 99.9% average uptime.

The V3 transition is the capacity-economics point. V2 satellites are shown at 96Gbps each, 27 satellites per Falcon 9 launch, and 2,600Gbps per launch. V3 satellites are shown at 1,024Gbps each, 60 satellites per Starship launch, and 61,000Gbps per launch.

Starlink Mobile targets terrestrial dead zones

Starlink Mobile is framed around about 30 mobile network operators, 5G connectivity to unmodified phones and IoT devices, about 1.9B people covered, 65MHz of spectrum, and roughly 650 V1 mobile satellites. V2 mobile satellite deployment is targeted for 2027.

The model is closer to complementing mobile carriers in hard-to-serve areas than replacing every terrestrial network. Spectrum transfers and regulatory approvals remain important conditions.

The highest-premium part of the story is AI compute

SpaceX ties xAI/Grok, real-time X data, and gigawatt-scale training clusters into the AI business. The deck cites 1GW of nameplate compute draw as of March 31, 2026 and large-scale GB200 and GB300 deployment.

The boldest claim is orbital AI compute. The logic is solar energy in space, radiative cooling, Starlink data routing, reusable Starship deployment, and faster chip-generation refresh cycles. If it works, SpaceX could bypass part of the terrestrial power bottleneck. If it does not, the most expensive option value in the roadshow gets repriced first.

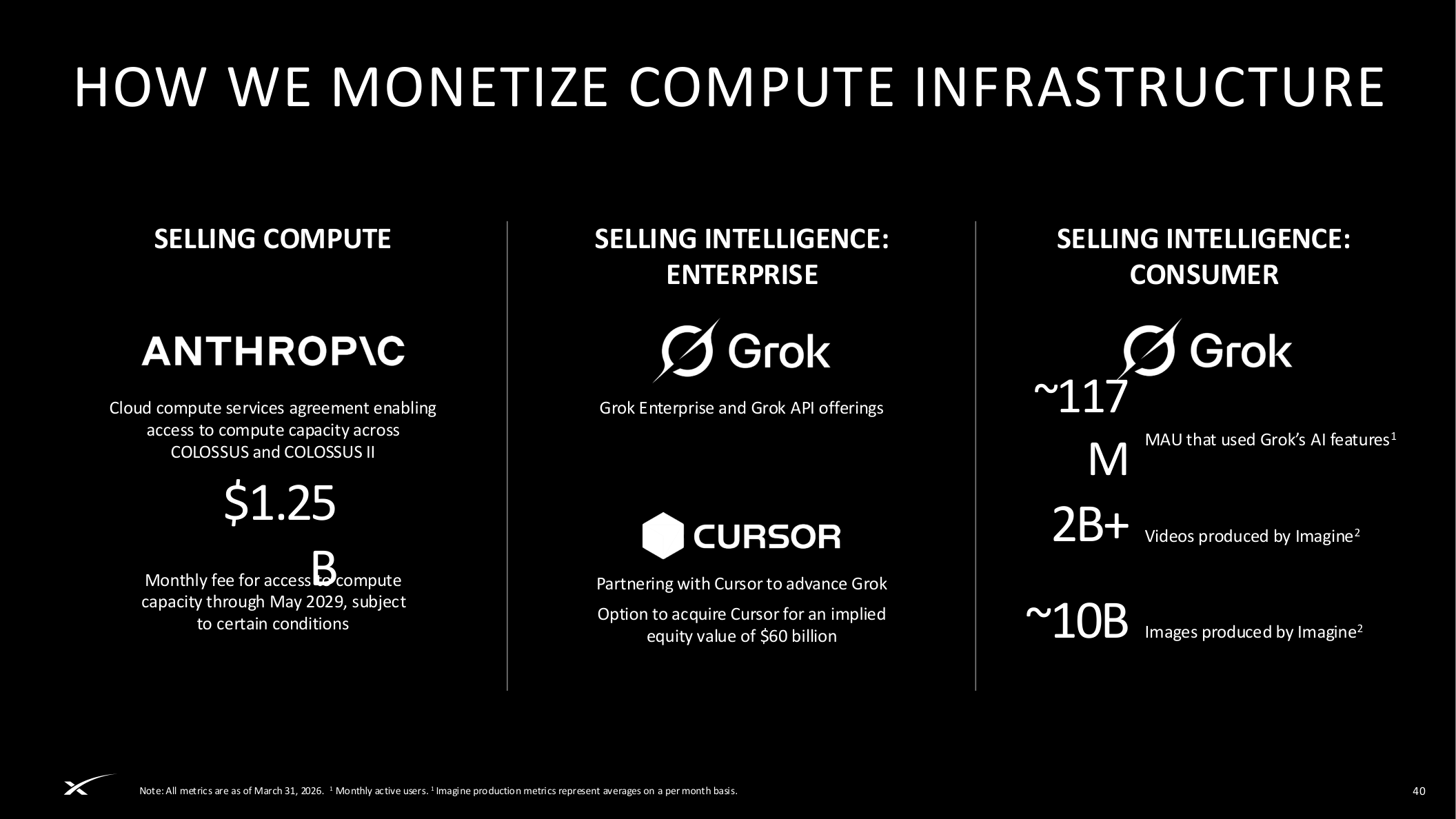

AI monetization runs through consumers, enterprise, and compute

The roadshow describes roughly 117M MAU using Grok AI features, 2B+ Imagine videos, 10B+ Imagine images, Grok Enterprise/API, a Cursor partnership, and access to compute capacity across Colossus and Colossus II. One cloud compute services agreement is described as a potential $1.25B monthly fee through May 2029, subject to conditions.

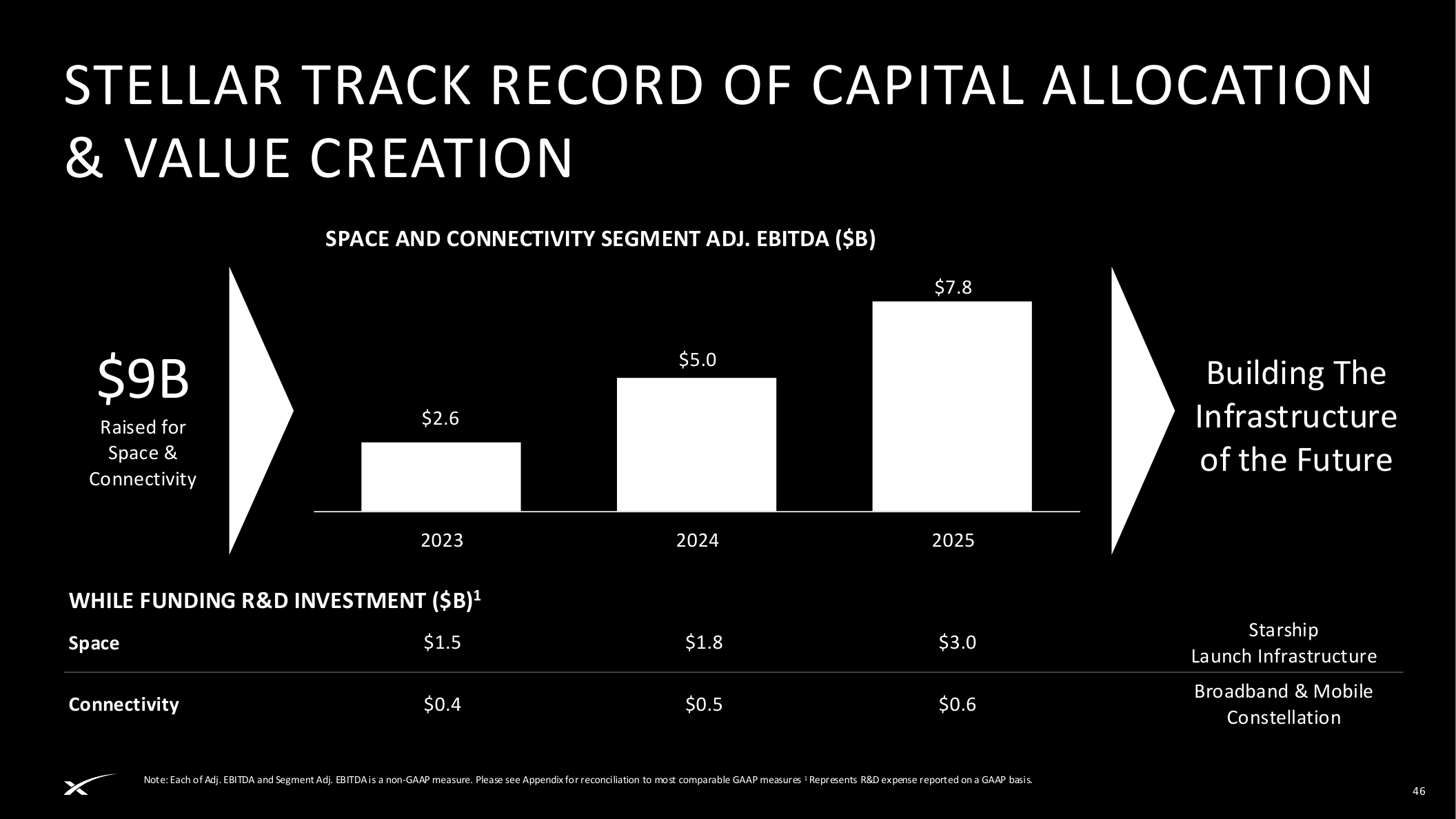

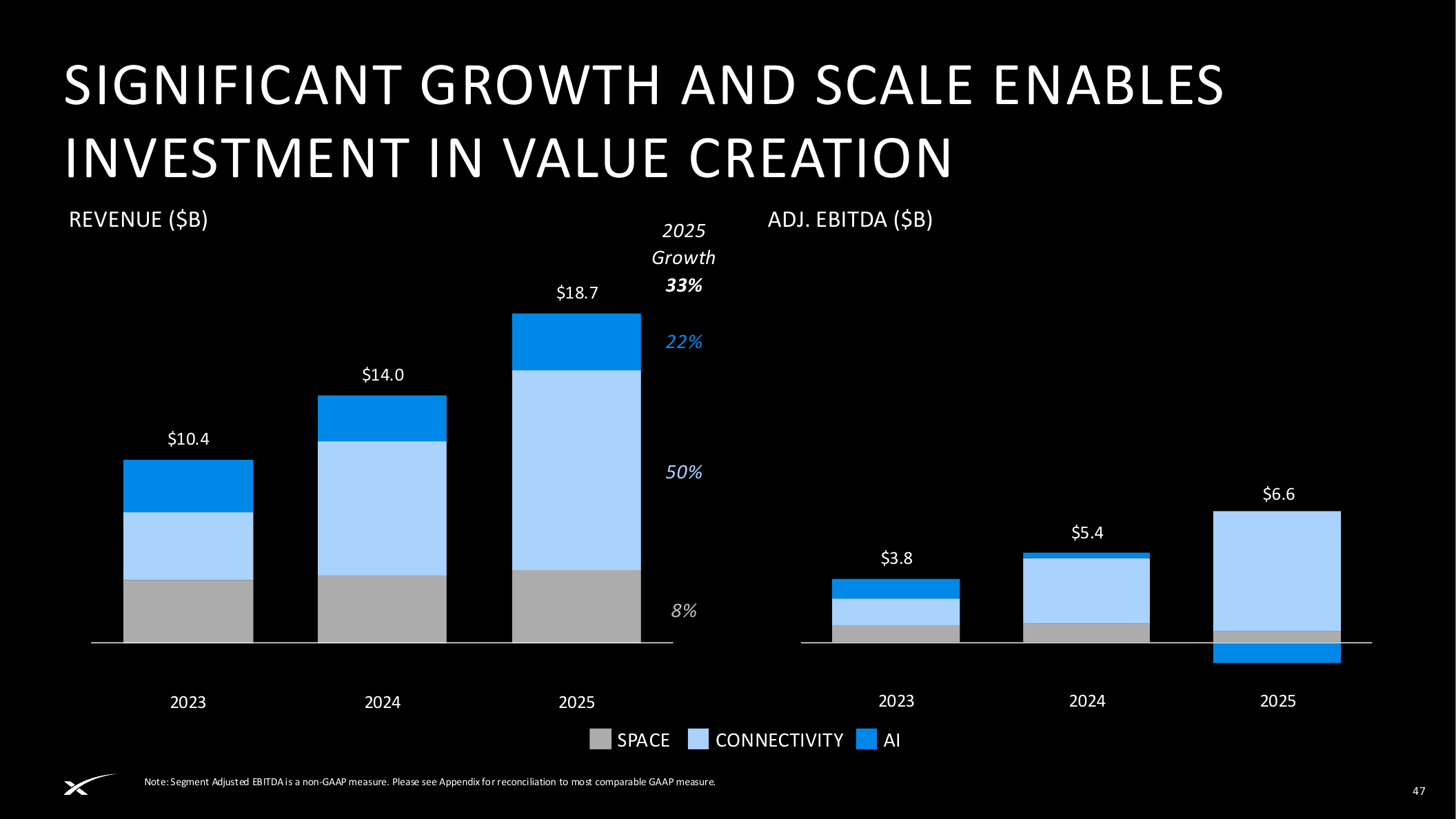

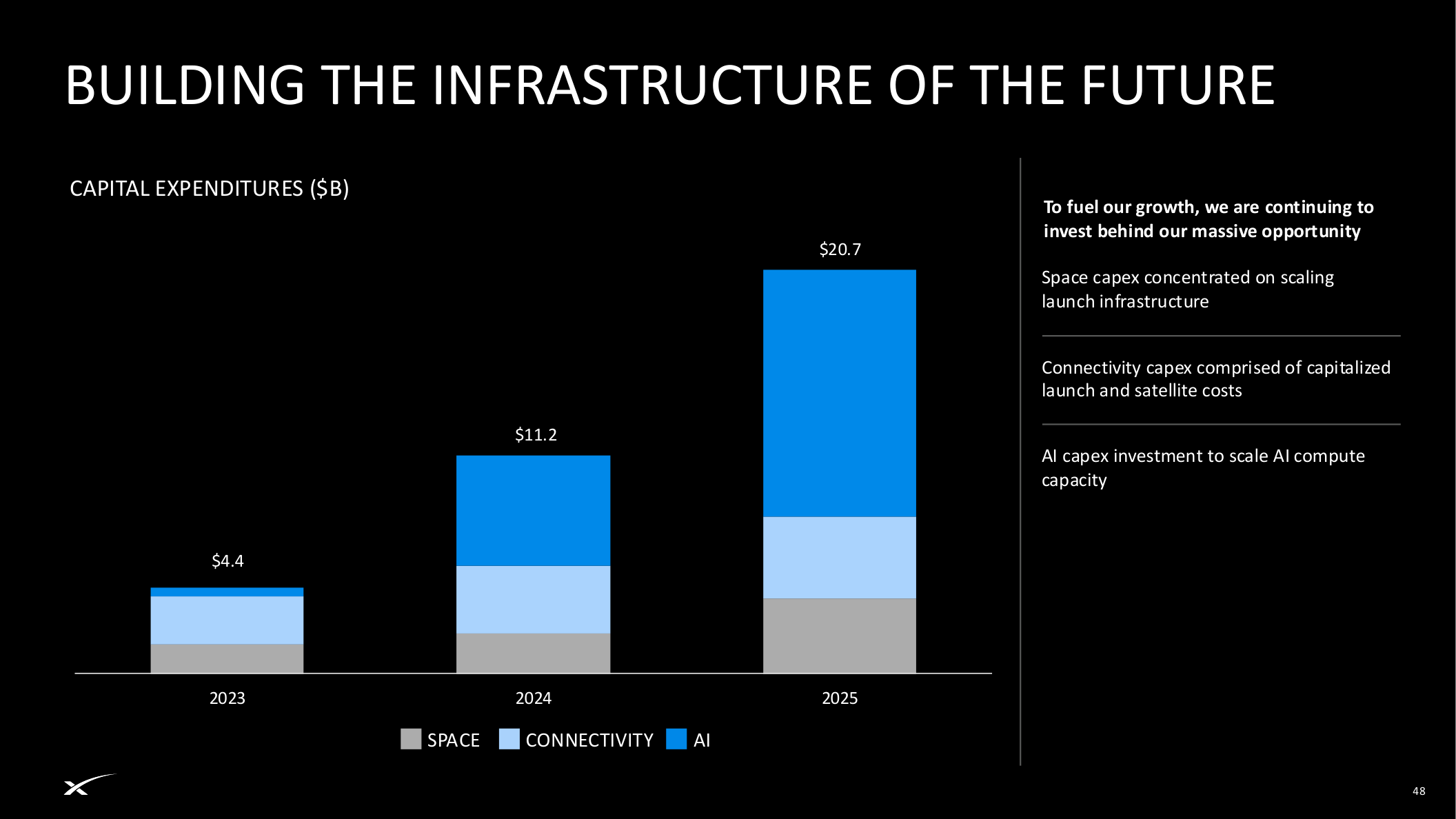

Space and connectivity produce EBITDA while AI absorbs investment

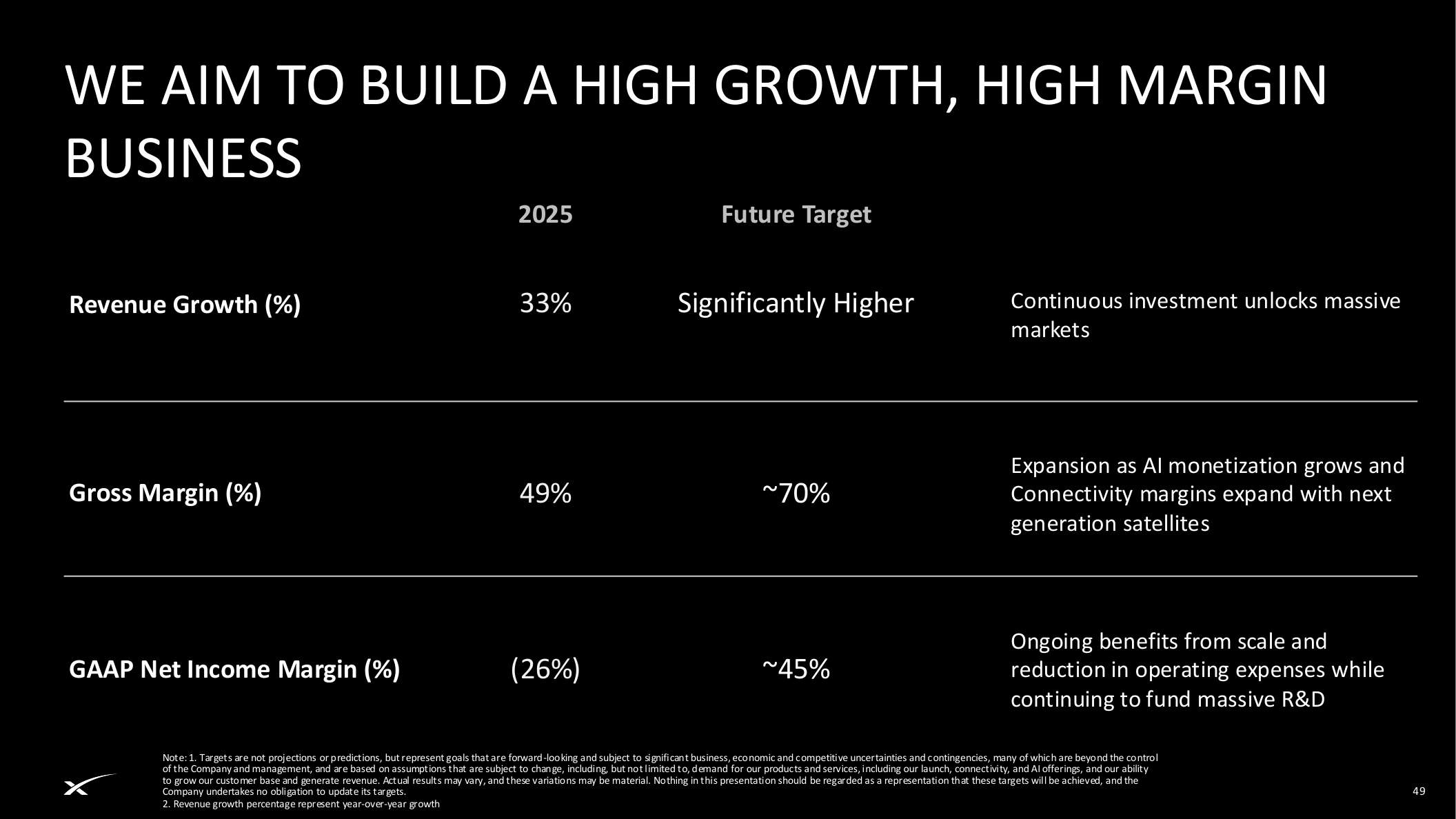

Space and Connectivity segment adjusted EBITDA is shown at $2.6B in 2023, $5.0B in 2024, and $7.8B in 2025. Total revenue is shown at $10.4B, $14.0B, and $18.7B for 2023-2025, while adjusted EBITDA is $3.8B, $5.4B, and $6.6B. Capex increased sharply from $4.4B in 2023 to $20.7B in 2025.

Five questions to monitor

- Starship economics: can high-cadence, low-cost, high-mass launch actually be delivered?

- Starlink ARPU and subscriber growth: can capacity gains offset global ARPU dilution?

- AI compute recurring revenue: can compute access, Grok Enterprise/API, and consumer AI features become repeatable revenue?

- Orbital AI compute evidence: power, cooling, communications, radiation, maintenance, and regulatory risks remain large.

- Lock-up and capex cycle: staged 2026-2027 lock-up releases and heavy capex can shape post-IPO supply and sentiment.

The IPO is a claim on physical infrastructure for the AI era

The SpaceX IPO story cannot be reduced to launch market share. The company is arguing that lower space-access cost enables Starlink connectivity, which enables data and customer relationships, which then feed AI compute and model monetization.

The key question is whether Starship, Starlink, xAI/Grok, and orbital compute can become one economic flywheel. If Space and Connectivity provide cash flow and AI compute becomes repeatable revenue, the premium has a coherent path. If Starship timing slips or orbital compute remains unproven, the richest option value in the story should be discounted first.

Korean version: Read the Korean version

This is a market interpretation based on public roadshow materials. It is an analytical framework for readers to compare against final offering documents and their own risk limits.

Public source checked

This article summarizes the company claims and figures in the SpaceX IPO Roadshow Presentation, June 2026. Any final investment decision should also review the SEC S-1, final pricing, risk factors, lock-up schedule, and post-listing financial disclosures.