COMPANIES · STREAMING · GROWTH × LIQUIDITY

Reading Netflix Again: Separate Moat, Price, and Timing

Netflix should be read through three separate questions: is the business still strong, is the price now reasonable, and is the timing attractive enough to act today?

1. Bottom line: strong business, but position sizing still matters

Netflix remains one of the rare global consumer platforms with brand, recommendation data, payment habits, distribution scale, and pricing power. That does not mean every pullback is an immediate full-position entry. Company quality, price, and timing should be separated.

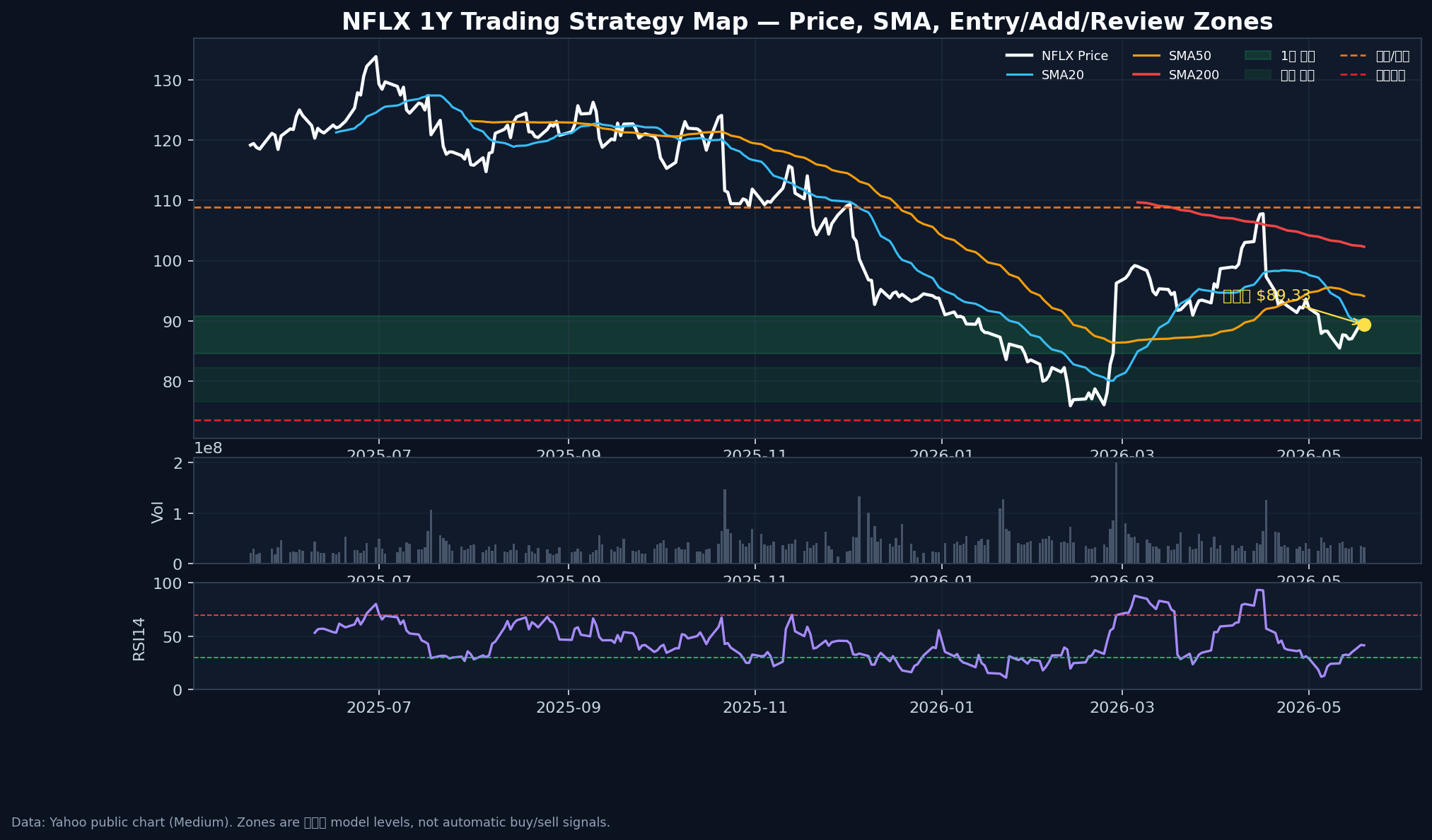

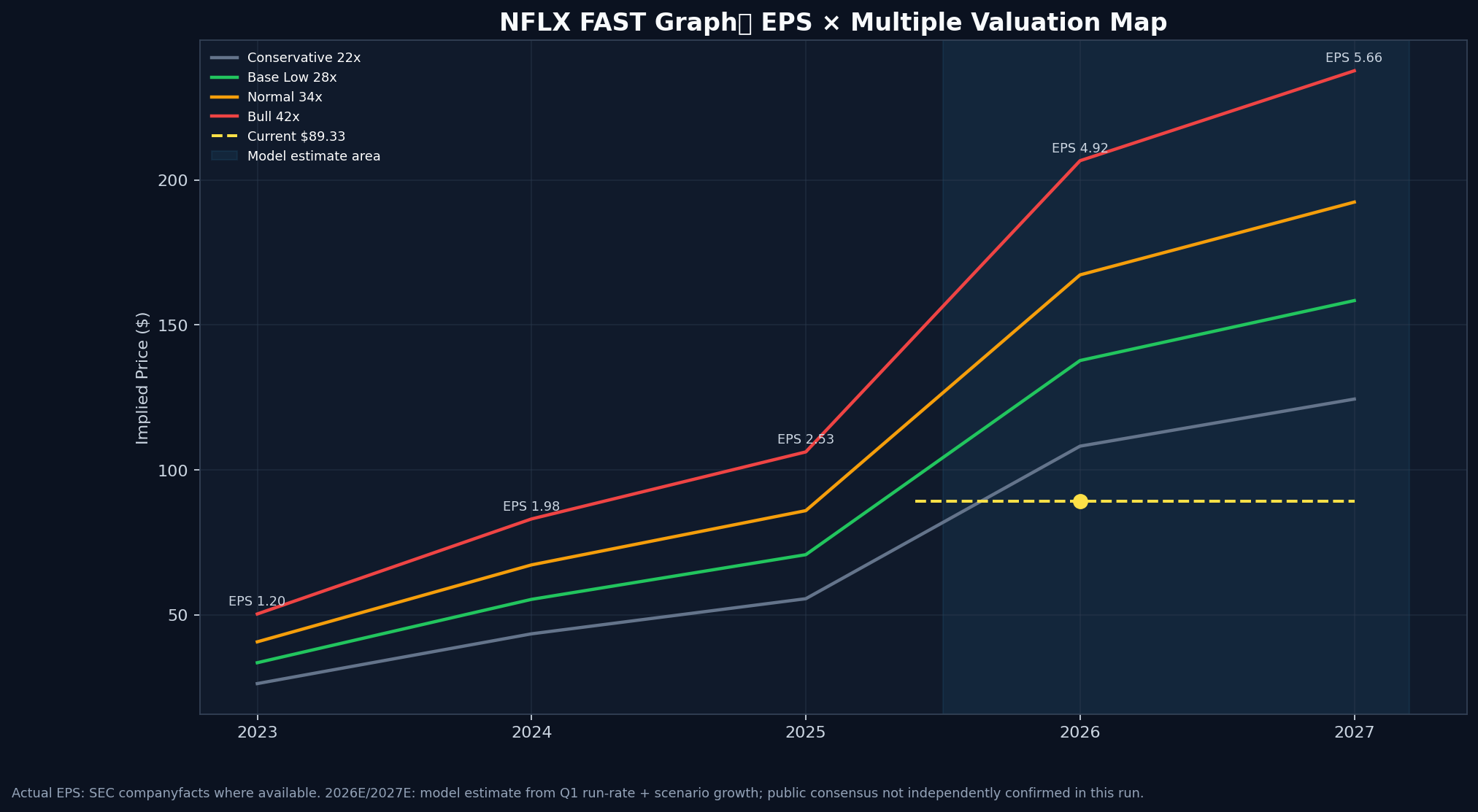

The report uses a Yahoo public chart reference price of $89.33. The stock is roughly one-third below its 52-week high and still below the 200-day moving average. That makes it a watchable candidate, not a reason to chase without confirmation.

2. Business: Netflix’s moat is more than content

The moat is not just a few hit shows. It is the operating system around global users, viewing data, recommendations, billing, local production, and pricing experience. Competitors can produce hits; fewer can repeatedly convert attention into profitable global scale.

The key questions are churn after price increases, monetization of the ad tier, content return on cash flow, and the real contribution of live events or gaming options.

3. Price: a large drawdown is a reason to study, not a full answer

A sharp decline from the high can create opportunity, but drawdown alone is not margin of safety. Valuation matters only if margins, cash generation, and advertising/pricing power continue to show up in results.

The setup looks less overheated than before, but it is not a simple “cheap at any price” case. The market already prices in some improvement from ads and margin discipline.

4. Timing: below the 200-day average, rules matter more than conviction

The chart shows a rebound attempt, but the long-term trend has not fully repaired. RSI14 is not deeply oversold, so the better approach is staged observation and confirmation rather than emotional averaging down.

5. What to monitor next

- Whether the ad tier becomes visible in revenue and margin

- Whether churn stays contained after price increases

- Whether content spending pressures free cash flow

- Whether SMA50/SMA200 recovery comes with volume

- Whether market liquidity supports growth-stock multiples

Netflix is a high-quality attention platform, but high quality does not remove the need for price and timing discipline. The useful question is not simply “is Netflix good?” It is whether the business, valuation, and action rule line up at the same time.

6. Portfolio role: quality growth, not a blind full-position entry

For a customer portfolio, Netflix should be treated as a profitable growth platform that still depends on market liquidity and valuation discipline. It is not an early-stage loss-making story, but it is also not immune to multiple compression when rates, growth-stock sentiment, or earnings expectations move against it.

The key question is no longer whether the company can survive. Netflix has already proven scale and profitability. The next question is whether advertising, pricing, content efficiency, and cash flow can support the valuation investors are asked to pay today. If those signals improve while the stock remains below prior enthusiasm levels, the drawdown can become useful. If the signals weaken, the lower price may simply be the market repricing slower growth.

7. Action rule: use evidence, not admiration

A practical action rule is to start small, add only when evidence improves, and review the position if the business signals deteriorate. A lower price alone is not a reason to add; better evidence at a reasonable price is. Similarly, a rebound alone is not confirmation unless earnings expectations, volume, and trend recovery support it.

The review conditions are also clear: slower ad-tier progress, higher churn after price increases, rising content cost pressure, or failure to reclaim long-term moving averages. If several of these appear together, the issue is not volatility; it is a weaker thesis.

That is the clean way to read Netflix now. The business remains strong enough to deserve attention, but the entry decision should be staged around price, evidence, and timing rather than admiration for the brand.

Source-use standard: SEC/company data is treated as high-confidence context; Yahoo public chart and auxiliary market data are used as public price references. Figures can change with the data timestamp.