Why Expensive Growth Stocks Can Stall: Tesla, Palantir and 13 High-Valuation U.S. Narratives

Tesla and Palantir carry some of the strongest narratives in the U.S. growth-stock universe. Yet a strong business story does not automatically translate into a strong stock return. When the market has already priced in two or three years of success, even a high-quality company can stall.

Korean version: /high-valuation-us-growth-stocks-tesla-palantir-2026/

The core question is simple. The issue is not whether these are good companies. The issue is how much future success has already been pulled into the current price. A moat can be real and still produce a poor entry point if the multiple is too demanding.

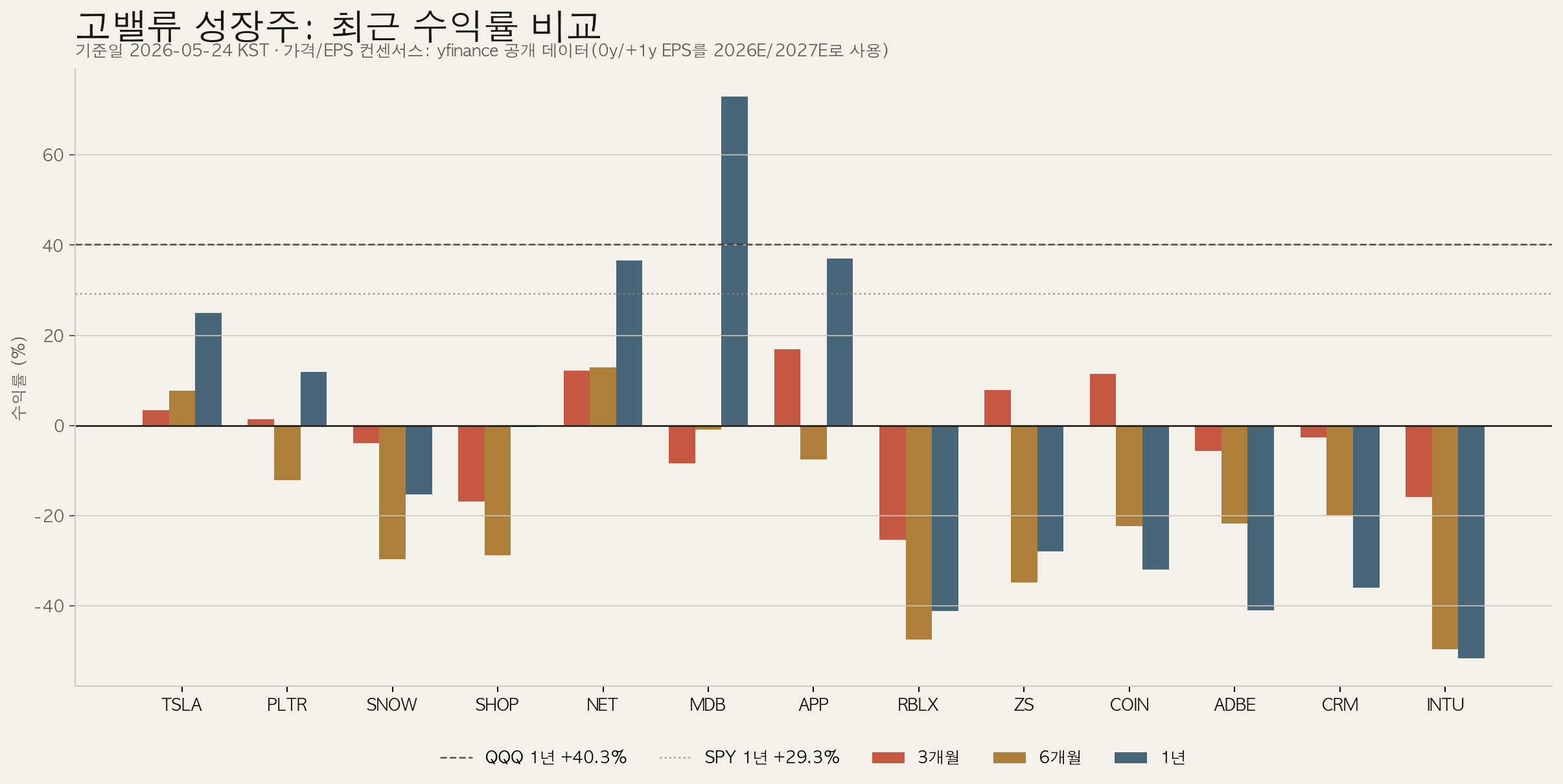

High-valuation growth stocks: return and P/E snapshot

The chart and visual board compare 13 U.S. growth names, including Tesla and Palantir, across 3-month, 6-month and 1-year returns plus 2026E and 2027E P/E estimates.

Narrative and business moat by company

Not every expensive growth stock has the same kind of story. Some are physical-AI platforms; others are data, security, commerce, creative workflow or crypto-infrastructure platforms. The key question is not only whether the story is large, but whether the business has a moat that can convert the story into revenue, margin and cash flow.

| Company | Narrative | Business moat | Why price can stall |

|---|---|---|---|

| Tesla TSLA | From EV maker to physical-AI platform across FSD, robotaxi, Optimus and energy storage | Real-world driving data, vertical manufacturing, battery/power electronics, charging ecosystem, brand and capital access | The P/E is hard to justify on auto earnings alone; robotaxi and Optimus need to become measurable economics |

| Palantir PLTR | AI operating system for government, defense and commercial decision workflows | Ontology layer, security trust, government credibility, workflow embedding and high switching cost | Growth and margins are strong, but the AI premium is already large; dilution and budget cycles still matter |

| Snowflake SNOW | Data cloud evolving into an AI data platform | Data sharing network, governance, multi-cloud data layer and customer data lock-in | A high P/E in a decelerating-growth phase needs visible AI workload usage and consumption growth |

| Shopify SHOP | Commerce operating system for independent brands and merchants | Merchant ecosystem, app store, payments/logistics/ads extension and switching cost | Sensitive to consumption, margins and growth expectations; good execution may not be enough if the entry multiple is high |

| Cloudflare NET | Global edge network expanding into security, developer tools and AI inference infrastructure | Global edge footprint, CDN/security/developer platform bundle, traffic data and scale economics | The revenue multiple is demanding; long-term TAM needs near-term profit conversion |

| MongoDB MDB | Developer-friendly database layer for AI applications | Document model, Atlas managed cloud, developer mindshare and application data switching cost | The one-year return is strong but YTD is weak; the market needs proof of growth re-acceleration |

| AppLovin APP | AI advertising engine and performance-marketing optimization platform | Axon model, ad-performance feedback loops and campaign-efficiency data | Profitability improved, but expectations rose quickly; ad cycle and model durability remain key |

| Roblox RBLX | User-generated social gaming and virtual-economy platform | Creator network, user community, virtual economy and young-user base | The narrative is large but profitability proof is thin; cash flow and monetization matter more than P/E |

| Zscaler ZS | Zero Trust security cloud | Cloud-native security architecture, enterprise network embedding and security data plane | Security demand is durable, but competition and sales efficiency concerns compress the old SaaS premium |

| Coinbase COIN | Regulated U.S. crypto financial infrastructure | Brand trust, regulatory adaptation, trading/custody/staking infrastructure and institutional access | Earnings are cycle-sensitive; 2026E looks expensive while 2027E embeds normalization hopes |

| Adobe ADBE | Creative software defending and extending into generative-AI creation workflows | Creative Cloud standard, file-format/workflow lock-in and enterprise customer base | The multiple is now lower; the key is whether AI weakens or reinforces the moat |

| Salesforce CRM | CRM system expanding into enterprise AI-agent workflows | Customer data, sales workflow embedding, AppExchange and enterprise sales channel | This is less about overvaluation now and more about proving AI monetization amid slower growth |

| Intuit INTU | Tax, accounting and personal-finance data platform | TurboTax/QuickBooks brand, tax data and small-business accounting workflow lock-in | AI tax automation and competition pressure the story; the multiple is lower but growth trust must recover |

What the Growth × Liquidity lens shows

Growth: the stories remain powerful

AI, data, cybersecurity, commerce, crypto infrastructure, creative software and physical AI remain attractive long-term themes. Many of these companies have large TAMs and platform expansion potential.

Liquidity: the price already discounts a lot

When rates are high or risk appetite weakens, the market becomes less willing to pay for earnings far in the future. Companies trading above roughly 50x forward earnings must keep proving that growth, margin and cash flow can catch up with the multiple.

Wait-list versus watch-list

Wait-list candidates

TSLA, PLTR, SNOW, SHOP and NET have compelling narratives and real moats, but valuation still matters. Investors need evidence such as robotaxi unit economics, AIP commercial adoption, AI data consumption, commerce margin expansion and edge-inference monetization.

Watch-list candidates

RBLX, ZS, COIN, ADBE, CRM and INTU need different checkpoints: profitability, security-SaaS sales efficiency, crypto-cycle earnings, and whether generative AI weakens or reinforces existing workflow moats. For some, the multiple has already compressed; the question is now growth trust.

Signals that can restart re-rating

- Revenue growth holds above market expectations.

- Operating margin or free-cash-flow margin improves.

- AI products translate into paid usage, ARPU, retention or seat expansion.

- Stock-based compensation and dilution decline.

- Lower rates or stronger risk appetite reduce the discount-rate burden on long-duration growth assets.

Signals that require caution

- Revenue holds up but free cash flow fails to improve.

- AI announcements do not lead to pricing power or usage growth.

- Guidance weakens while the stock still trades at a high multiple.

- The long-term TAM narrative keeps expanding while near-term unit economics remain unclear.

Final view

Tesla and Palantir remain flagship narrative stocks. But the current market is less willing to reward a big story without numerical proof. High-valuation growth stocks must keep converting future promise into present evidence every quarter.

A great company bought at the wrong price can still produce a weak return. A great company that rests long enough can become the next-cycle candidate.

Price, return and EPS consensus fields are based on public yfinance data. The moat and narrative discussion combines each company’s public business model, product/platform/customer structure and the SignalnFlow Growth × Liquidity framework. This article is an investment interpretation, not a buy or sell instruction.