After CXMT, Is the Memory Supercycle Over?

AI has forced investors to re-rank software companies. Something similar is happening inside semiconductors. Memory used to be treated mostly as a cycle business tied to PCs and smartphones. But as AI data centers scale, the market is starting to ask a different question. The issue is no longer only whether DRAM prices are rising. The issue is who can solve the memory bottleneck that AI infrastructure now creates.

That is why CXMT’s listing push and prospectus matter. China’s largest DRAM maker is no longer a distant footnote. It is becoming an industry variable. The question is whether Chinese DRAM supply can weaken the profitability of Samsung Electronics, SK hynix, and Micron — or whether the AI memory bottleneck is structurally harder to solve than adding commodity DRAM capacity.

The short answer is this: CXMT is a real threat, but its near-term pressure is more likely to appear in commodity DRAM than in the core of HBM.

The DRAM segment that Chinese supply can pressure and the memory layer for which AI infrastructure pays a premium are not the same market.

Prices Are Already Reflecting the AI Memory Bottleneck

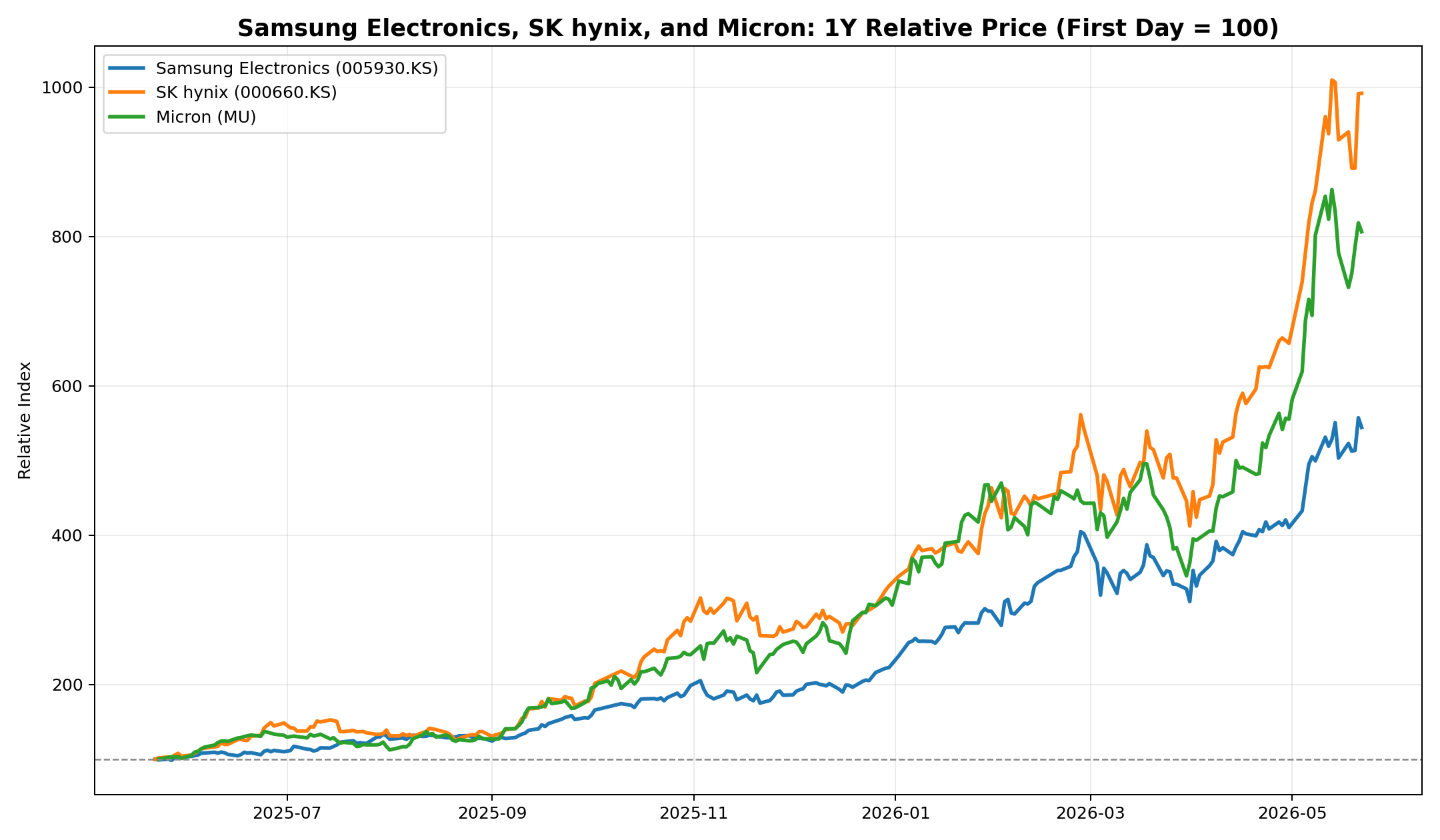

Over the past year, the major memory stocks have been strongly re-rated. Based on public price data, Samsung Electronics, SK hynix, and Micron all rose sharply.

| Company | Ticker | Window | 1Y return | 6M return | 3M return |

|---|---|---|---|---|---|

| Samsung Electronics | 005930.KS | 2025-05-22 → 2026-05-22 | +444.2% | +192.8% | +54.2% |

| SK hynix | 000660.KS | 2025-05-22 → 2026-05-22 | +891.5% | +221.1% | +104.9% |

| Micron | MU | 2025-05-23 → 2026-05-22 | +706.3% | +273.3% | +79.7% |

This is not just a cyclical bounce. The market is no longer looking at memory only as a component tied to PC and smartphone replacement cycles. As AI clusters grow, GPUs are not the only constraint. HBM, server DDR5, high-capacity modules, power, and thermal constraints all become part of the bottleneck.

That does not mean the trade is easy from here. When price moves first, expectations rise with it. Investors now need evidence that each company can convert HBM and server-memory scarcity into revenue, margins, and durable customer relationships.

What CXMT’s Prospectus Really Shows

CXMT’s prospectus makes the company’s position clearer. The company focuses on DRAM research, design, manufacturing, and sales. It highlights the adoption of DDR5 and LPDDR5/5X products. It also positions itself as China’s largest DRAM maker and a global No. 4 player by capacity.

But the prospectus also shows the limits. CXMT still acknowledges a capacity gap with the top three global producers. It also explains that since the second half of 2025, global computing demand and capacity allocation by major producers have tightened DRAM supply and pushed prices sharply higher.

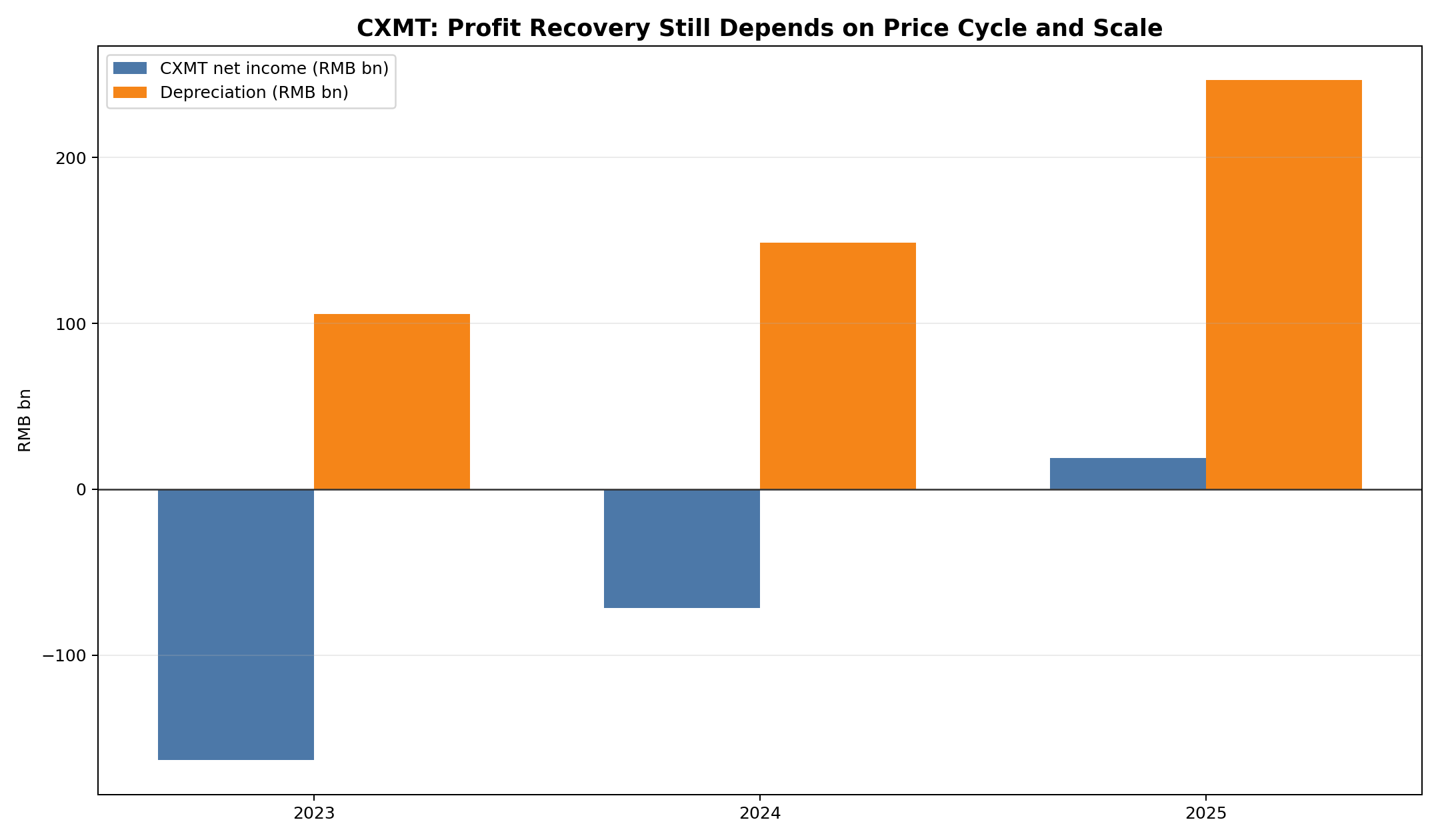

The financials reveal the core nature of the memory business.

| Item | 2023 | 2024 | 2025 |

|---|---|---|---|

| Net income | -RMB 16.34bn | -RMB 7.14bn | +RMB 1.87bn |

| Depreciation | RMB 10.56bn | RMB 14.88bn | RMB 24.68bn |

| Fixed assets / total assets | 43.8% | 56.4% | 54.3% |

| Inventory | RMB 14.18bn | RMB 21.21bn | RMB 29.39bn |

| Main DRAM ASP growth | – | +55.1% | +33.7% |

The eye-catching line is the return to profitability in 2025. But the more important line is depreciation. CXMT’s depreciation expense was far larger than its net income. This is why memory remains a brutally capital-intensive industry. When the price cycle turns down, inventory and depreciation can pressure earnings quickly.

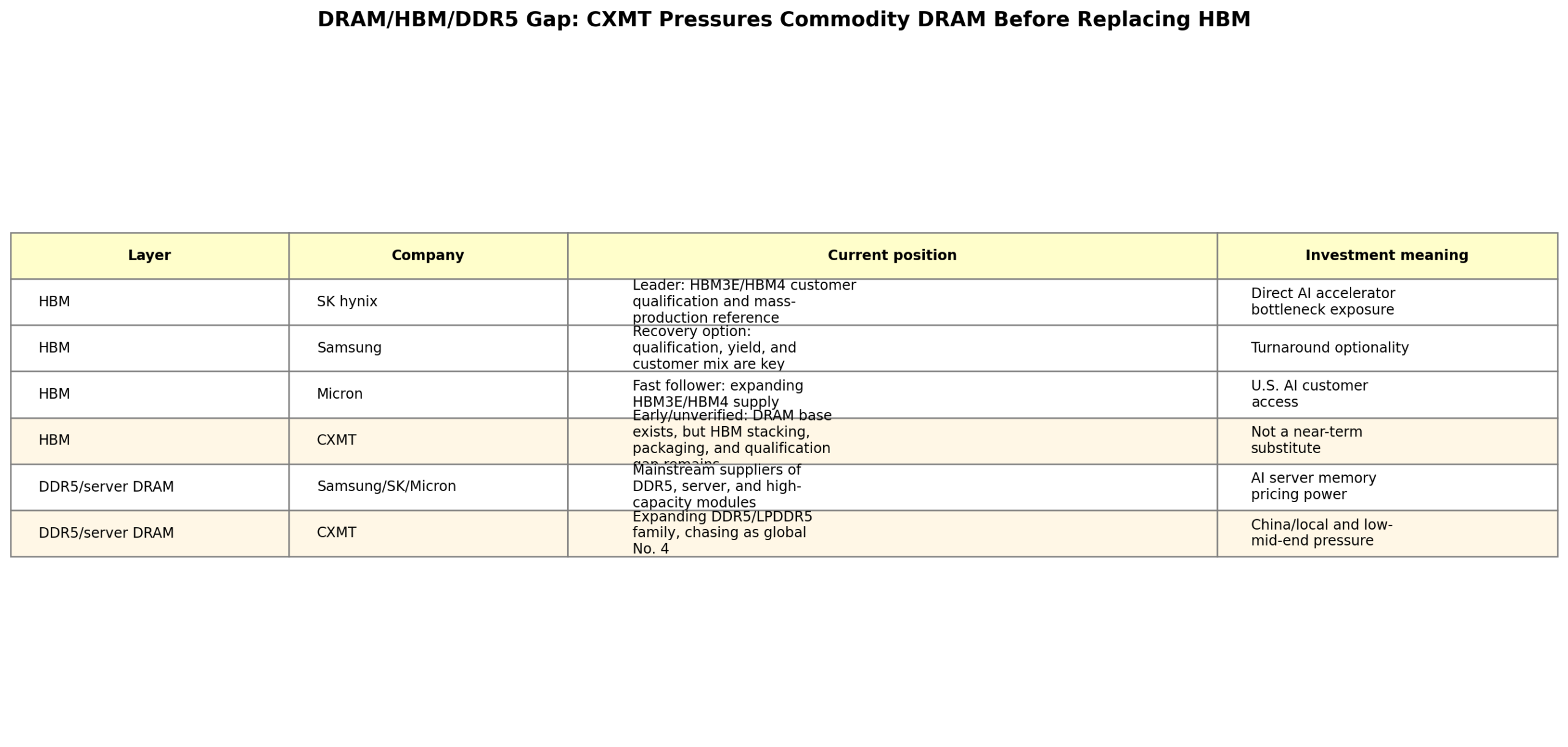

CXMT Pressures Commodity DRAM Before It Replaces HBM

The biggest mistake is to say, “Chinese DRAM is growing, so the HBM bottleneck will soon disappear.” DRAM is one word, but commodity DRAM and HBM have very different economics.

HBM is not created simply by adding wafer capacity. It requires high-stack integration, TSV, advanced packaging, thermal control, yield, customer qualification, and co-optimization with GPU and ASIC platforms. For AI accelerators, performance matters, but reliability, timing, and supply confidence matter just as much.

Based on public materials, SK hynix, Samsung Electronics, and Micron are all emphasizing HBM3E, HBM4, high-capacity server memory, and AI customer collaboration. CXMT is moving faster in DDR5 and LPDDR5-class products, but public evidence of HBM mass production and customer qualification remains limited.

That means CXMT’s near-term impact is not likely to be direct HBM substitution. A more realistic impact is pressure on commodity DRAM pricing, higher China-local substitution, and long-term pressure on the lower-value portions of the incumbents’ product mix.

Has the Market Misunderstanding Been Resolved?

When AI narratives first emerge, the market often starts with broad claims: existing businesses will be destroyed, or all incumbents will be replaced. Over time, the market becomes more selective. Some companies lose pricing power because of AI. Others become more important because they control a bottleneck.

Memory is following the same pattern. The rise of Chinese DRAM is a real risk. But it does not automatically remove the AI memory bottleneck. Commodity DRAM supply growth and HBM scarcity belong to the same industry, but they are not the same investment variable.

So has the misunderstanding been resolved? Half yes, half no.

The resolved part is clear. The market now understands that AI server memory is not just another semiconductor component. It is a bottleneck asset. That is visible in the re-rating of SK hynix and Micron, and in the recovery option embedded in Samsung’s HBM story.

The unresolved part is the tendency to compress commodity DRAM and HBM into one cycle. CXMT’s expansion can pressure commodity DRAM, but public evidence does not yet support the idea that it can quickly remove the HBM qualification bottleneck.

Do Not Put the Three Memory Companies in One Basket

SK hynix: Premium From HBM Leadership

SK hynix has the clearest HBM leadership. A company with customer qualification and mass-production reference is not just selling memory; it is solving a platform bottleneck. In this layer, reliability, yield, delivery timing, and co-optimization can matter more than spot price.

This makes SK hynix a core-candidate name, but price discipline matters after such a large move. The next questions are HBM4 transition, customer mix, margin durability, and whether pricing can hold as supply expands.

Samsung Electronics: The Largest Recovery Option

Samsung has the widest set of options. It can connect DRAM, NAND, foundry, packaging, and system semiconductors. If Samsung regains HBM customer trust and yield credibility, the re-rating potential is meaningful.

But the investment question is not simply whether Samsung is cheap. The key evidence is whether HBM customer confidence is returning and whether partnerships with customers such as AMD translate into volume and margins. Samsung looks more like a wait-to-add candidate until those signals strengthen.

Micron: U.S. AI Supply-Chain Premium

Micron is being revalued as a supplier to the U.S. AI infrastructure chain. Its public HBM materials emphasize HBM4 36GB 12H, more than 11Gb/s pin speed, and more than 2.8TB/s bandwidth. The message is that Micron is no longer being viewed only as a commodity-memory company.

The risk is that Micron remains cyclical and the valuation re-rating has moved quickly. As long as U.S. AI capex remains strong, the story can continue. But when expectations are already embedded in price, earnings disappointments can hurt.

CXMT: More an Industry Variable Than a Direct Investment Target

CXMT is not yet a listed public-market stock. For most investors, it is better treated as an industry variable than as a direct investment target. China-local DRAM substitution, commodity pricing pressure, and long-term technology catch-up are real risks. But the public evidence is not enough to say that CXMT will quickly solve the HBM bottleneck.

Five Signals to Watch Next

First, HBM4 customer qualification. The most important question is who wins confirmed volume on next-generation AI accelerator platforms.

Second, commodity DRAM ASP. Investors need to watch how much CXMT and China-local capacity pressure PC, mobile, and mainstream server DRAM prices.

Third, how much HBM capacity crowds out ordinary DRAM. HBM is high-value, but capacity allocation matters. More HBM can also mean tighter supply for conventional DRAM.

Fourth, depreciation and inventory. CXMT’s prospectus shows how quickly memory earnings can be pressured when price weakens and fixed costs remain high.

Fifth, the quality of AI capex. GPU orders are not enough. Actual cluster buildout, power availability, utilization, and inference demand determine how long the memory bottleneck premium can last.

The Real Question

CXMT is a threat to the incumbent memory companies. But the threat begins in the lower layers of DRAM before it reaches the heart of HBM.

The question is not simply, “Will Chinese DRAM hurt the memory cycle?” The better question is:

How long can the premium from AI memory bottlenecks overcome the pressure from commodity DRAM supply?

The market’s answer so far is clear enough. AI memory scarcity has been priced aggressively. But the misunderstanding is not fully gone. The likely winners are not the companies that make the most DRAM. They are the companies that can reliably supply the memory AI customers need first.

Source-use standard

This article is based on CXMT’s prospectus, official product and news announcements from Samsung Electronics and Micron, and public price data. Return figures are simple returns between the stated reference dates and the latest available close checked for this article. Future performance will depend on HBM customer qualification, average selling prices, supply growth, and the durability of AI infrastructure investment.