AI VALUE CHAIN · SIGNAL & FLOW

Who Makes Money in the AI Value Chain: The Moat Is Control of the Bottleneck, Not the GPU

Companies shown in the maps are examples for understanding the value chain. OpenAI and Anthropic are included as non-public demand actors for context. The valuation map is an interpretive visualization based on public consensus metrics, not a recommendation to buy or sell any security.

1. Change the question

The usual question is, “Which companies benefit from AI?” That is too broad. A better question is: as AI demand grows, which bottlenecks become more valuable—and who controls them?

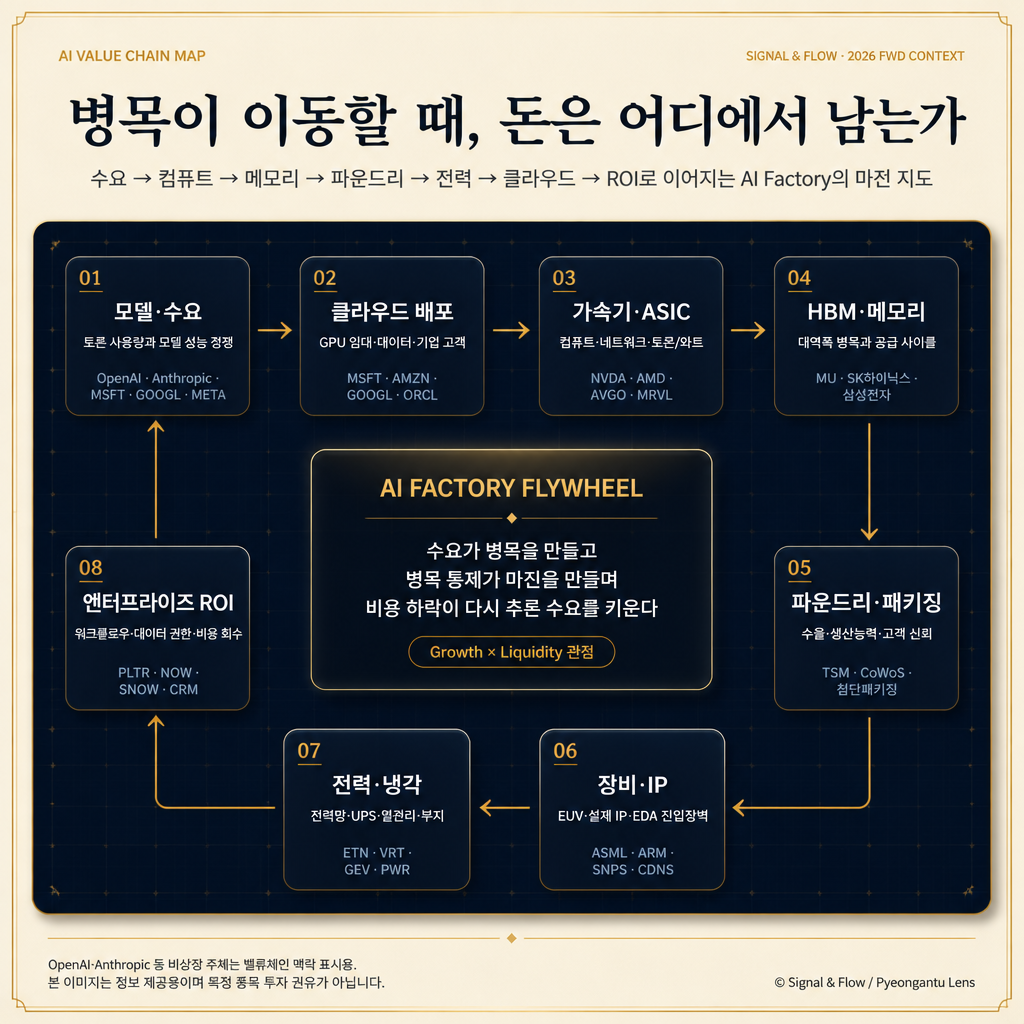

The AI value-chain moat can be divided into four layers: compute architecture, manufacturing and packaging, cloud distribution, and ROI capture inside enterprise workflows. Bottlenecks migrate from GPUs to HBM, CoWoS, networking, rack systems, power, cooling, cloud capacity, security, and enterprise permissions—but they do not disappear.

2. NVIDIA is a system standard, not just a GPU vendor

NVIDIA’s moat is not only GPU performance. It is the full system: GPU, CPU, memory, networking, racks, software, developer ecosystem, and token-per-watt economics. CUDA raises switching costs. Networking and rack-level design matter more as clusters scale. Power constraints make total cost of ownership more important than chip benchmarks alone.

3. TSMC and ASML are physical scarcity moats

AI may be a software revolution, but frontier models still run on physical semiconductors. TSMC’s moat is trusted leading-edge manufacturing, yield management, advanced packaging, and customer confidence. ASML’s moat is even more direct: EUV remains one of the hardest bottlenecks in advanced semiconductor manufacturing.

4. Custom silicon, IP, memory, and cloud distribution

Broadcom and Marvell sit in the custom ASIC and networking layer. Arm monetizes IP royalties where power efficiency matters. Micron benefits from the HBM cycle, but memory remains more cyclical than a permanent monopoly. Microsoft, Alphabet, Amazon, and Meta convert AI infrastructure into monetization through cloud, software contracts, ads, user data, and distribution.

5. Enterprise software and power infrastructure

Palantir, ServiceNow, Snowflake, and Salesforce are not valuable because they own foundation models. Their moat is access to enterprise data and workflows. Eaton, Vertiv, and GE Vernova benefit from the physical power and cooling constraints of AI data centers, but their economics remain project-cycle sensitive.

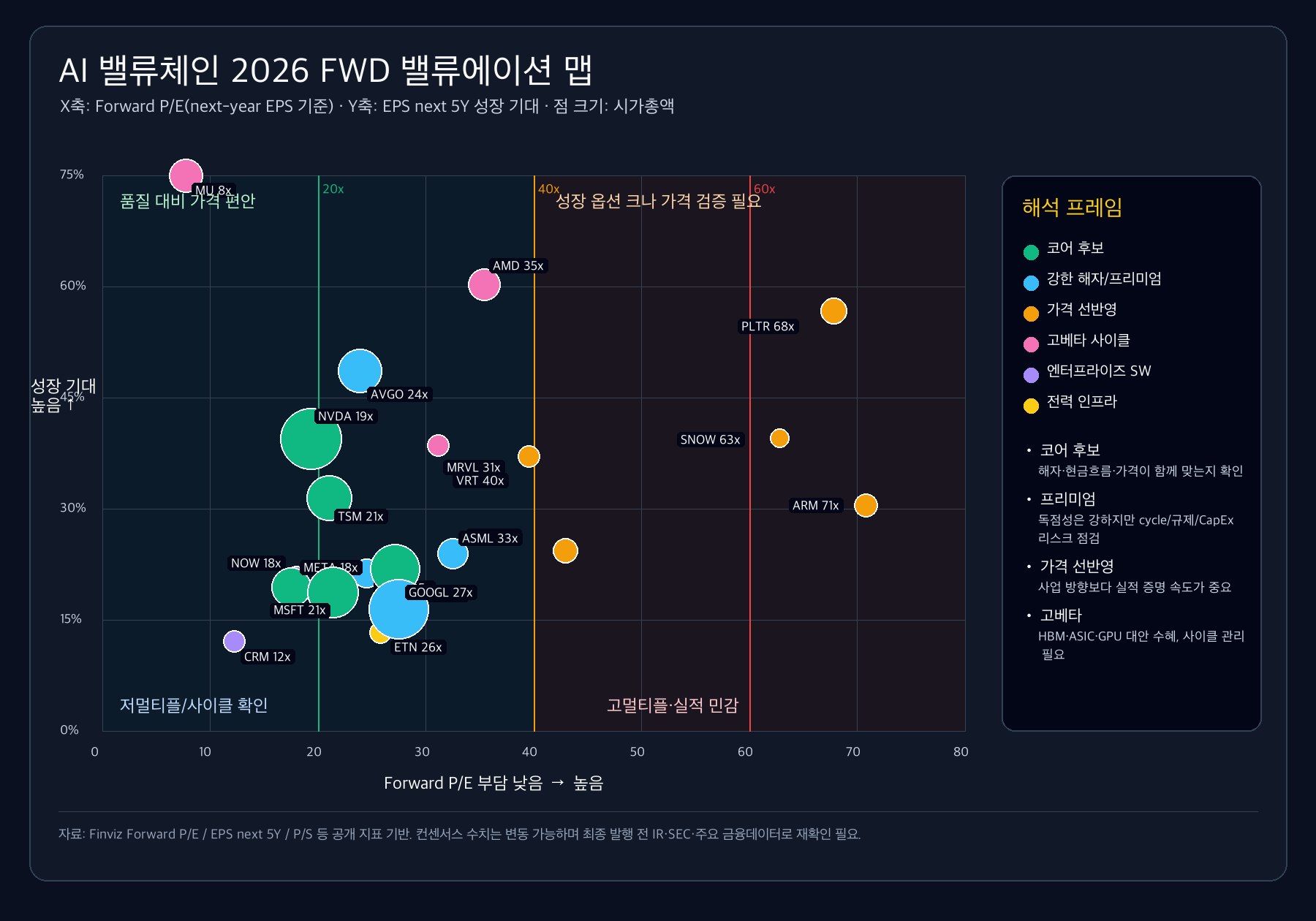

6. The 2026 forward valuation map

The map separates four groups:

- Moat plus relatively comfortable price: NVIDIA, TSMC, Microsoft, Meta, Amazon.

- Strong moat with premium valuation: Broadcom, ASML, Alphabet, Oracle.

- Growth option priced ahead of proof: Arm, Palantir, Snowflake, Vertiv, GE Vernova.

- High-beta cyclical beneficiaries: Micron, AMD, Marvell.

The key lesson is simple: a good company and a good entry price are not the same thing.

7. What investors should monitor

1. Whether cloud customers can prove AI ROI fast enough.

2. Whether today’s bottlenecks become tomorrow’s oversupply.

3. Whether model/software differentiation weakens and value shifts to data, distribution, workflow, and customer lock-in.

Final view

The strongest structural moats remain around NVIDIA, TSMC, Microsoft, Alphabet, Amazon, and Broadcom. Meta looks relatively attractive when AI-driven ad efficiency is paired with cash flow. ASML remains a premium physical-bottleneck asset. Palantir, Arm, Snowflake, Vertiv, and GE Vernova have attractive directions but require stricter price discipline. Micron, AMD, and Marvell are high-beta AI cycle beneficiaries rather than default long-term core holdings.

The core question is not “who sells the GPU?” It is who controls the bottleneck of the AI economy and converts that control into recurring revenue and high margins.

How to read the data

This article combines public forward-valuation metrics, company IR/SEC materials, and Signal & Flow’s Growth × Liquidity / value-chain moat framework. Consensus numbers can change quickly, so readers should re-check current filings and financial data before making any investment decision.

Sources and basis: public Finviz forward valuation metrics, company IR/SEC materials, and Signal & Flow’s Growth × Liquidity / value-chain moat framework. This article is research commentary, not a recommendation to buy or sell any security.