Cerebras IPO: Semiconductor Momentum Is a Tailwind, but Price Discipline Still Matters

Cerebras is a useful test for whether the AI semiconductor leadership trade still has breadth. The bias can be constructive — but not price-insensitive. The company narrative and the entry price must remain separate decisions.

The constructive case

Cerebras should not be reduced to a simple “Nvidia rival” headline. The better frame is bottleneck migration: inference latency, memory bandwidth, networking, power, cloud procurement, and chip supply diversification. Signal & Flow’s AI semiconductor notes treat this cycle as a moving bottleneck map rather than a single-stock GPU story.

OpenAI-related notes also matter. OpenAI has signaled a broader compute supply strategy that includes AMD and Cerebras alongside Nvidia. If Cerebras can improve the spread between the economic value of tokens and the cost of producing them, part of the premium can be justified.

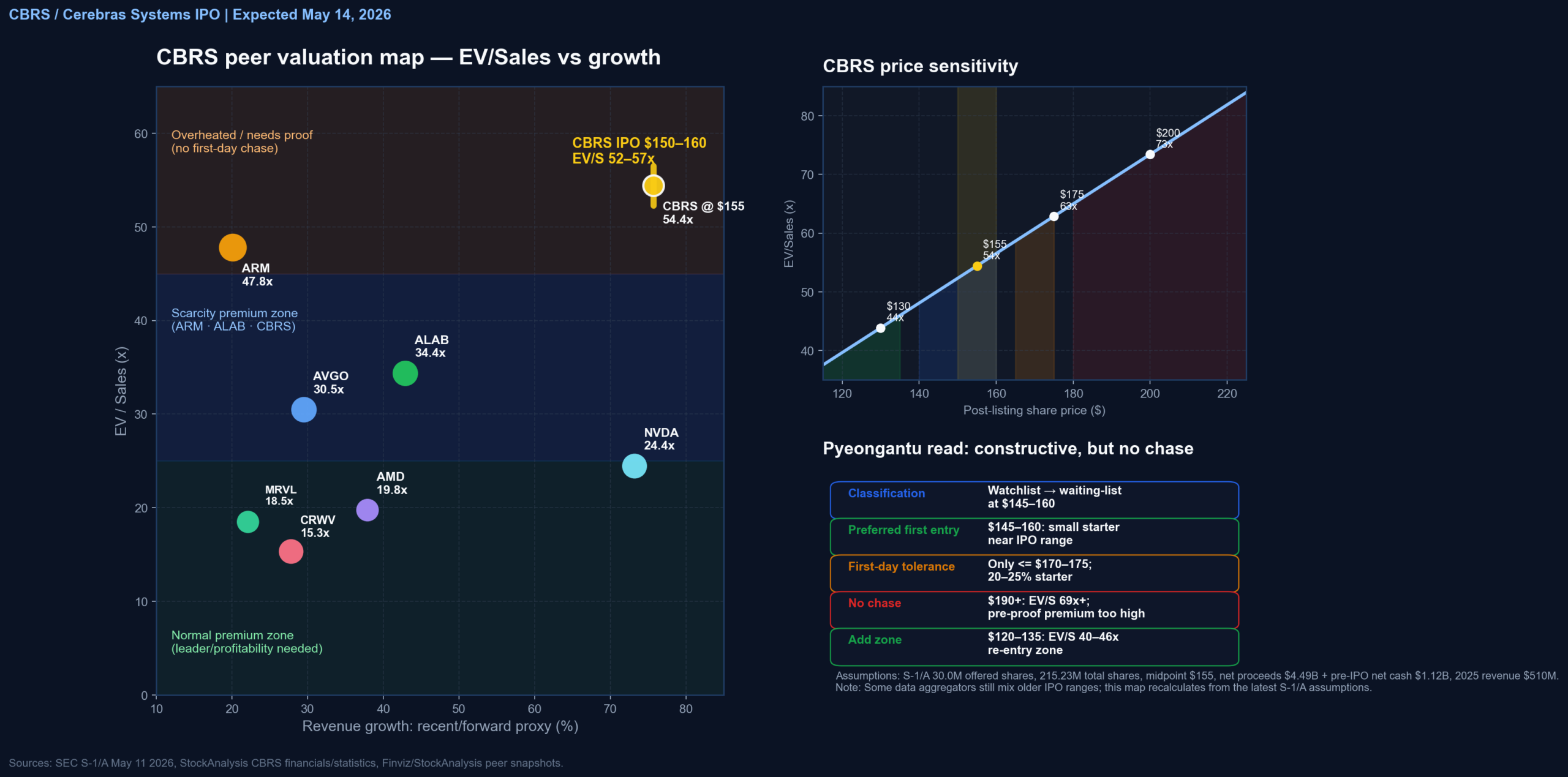

The valuation map

Based on the latest S-1/A and IPO data, the indicated range is $150–160 with 30 million shares offered. StockAnalysis shows 2025 revenue of about $510 million, 75.7% revenue growth, 39.0% gross margin, and -28.6% operating margin. Recalculated at a $155 midpoint, the implied EV/Sales is roughly 54x.

| Post-listing price | Read | Action |

|---|---|---|

| $120–135 | Attractive re-entry zone | Consider adding if the thesis remains intact. |

| $145–160 | Preferred first-entry zone | Small starter, around 20–30% of intended position. |

| $170–175 | Upper first-day tolerance | Only if semiconductor momentum and trading quality are strong. |

| $190+ | No chase | Premium becomes too rich before public-market earnings validation. |

Conclusion: The setup is positive, but the process should be disciplined. $145–160 is the preferred small-entry zone, $170–175 is only acceptable with strong tape, and $190+ should be allowed to pass.

Sources: SEC EDGAR Cerebras Systems Inc. S-1/A filed 2026-05-11; StockAnalysis CBRS overview/financials as of 2026-05-12 KST; Signal & Flow editorial research context. Not investment advice; final pricing, prospectus terms, lockups, and first-day trading data should be rechecked.